Hormuz closure offsets tariff reversal; U.S. left with upside inflation risk

A pair of important and opposing trade shocks hit the U.S. economy during the first quarter of 2026. The Supreme Court struck down a portion of the tariffs imposed under the International Emergency Economic Powers Act (IEEPA). The decision on Feb. 20 lowered average U.S. import tariffs by roughly 4.8 percentage points.

Weeks later, Iran’s closure of the Strait of Hormuz as part of the conflict in the Middle East not only affected oil prices by disrupting the supply of oil and petroleum goods, it also affected shipping flows, increasing costs along key routes. These two shocks—the decline in average U.S. import costs and the increase in global shipping costs—pull U.S. inflation in opposite directions. The relative magnitude of these shocks determines the path of core personal consumption expenditures (PCE) inflation through 2026.

Drawing on a model developed in recent research with the precise aim of understanding the effects of trade disruption on inflation dynamics, we seek to quantify the inflationary impact of the shocks and assess how they combine. We find that an increase in shipping costs due only to trade disruptions generated by the unexpected closure of the strait—independently of those generated by the subsequent increase in oil prices—completely undoes the disinflationary effects of permanently lower tariffs.

Thus, any additional forces putting upward pressure on core inflation, such as higher oil prices and their effects on shipping costs, would add to U.S. core (nonenergy and food) PCE inflation above and beyond 2026 forecasts made at year-end 2025.

IEEPA tariffs and their inflationary footprint

The IEEPA tariffs announced in April 2025 raised average U.S. import costs by approximately 12.1 percentage points and contributed roughly 0.8 percentage points to 12-month U.S. core PCE inflation by year-end 2025. Those tariffs and their expected permanence had become a meaningful component of the inflation backdrop embedded in economic forecasts for 2026.

The Supreme Court ruling did not undo the full 12.1-percentage-point increase. It struck down the IEEPA-specific portion, leaving other existing and new tariff measures in place, thus reducing the average effective tariff by about 4.8 percentage points. The relevant question for the inflation outlook is: How much will the removal of these tariffs contribute to unwinding U.S. inflation by year-end 2026?

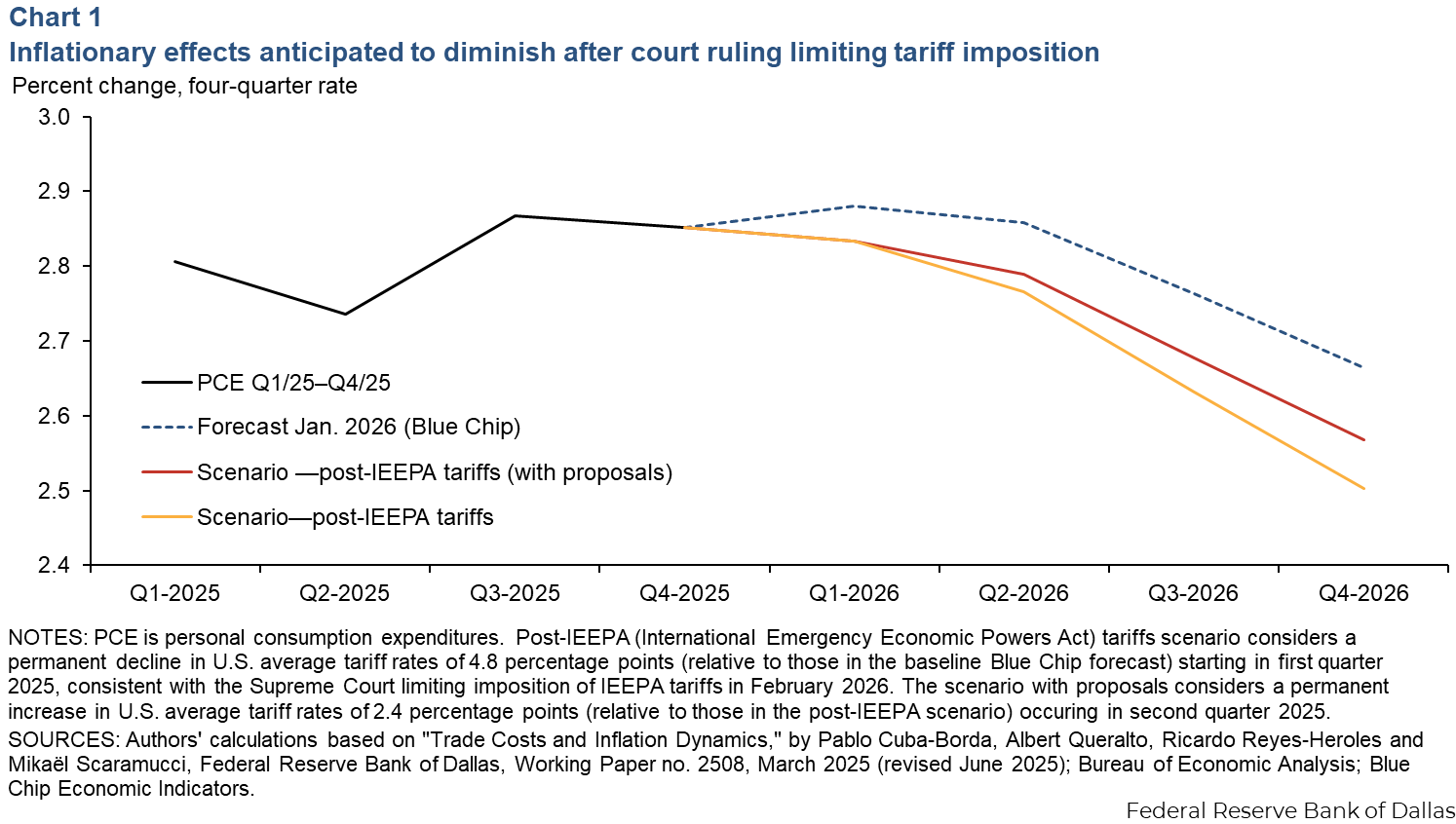

Chart 1 shows the model-implied path of four-quarter core PCE inflation under a permanent 4.8-percentage-point reduction in average import tariffs beginning in first quarter 2026 (orange line).

The model implies that the ruling lowers core PCE inflation by approximately 0.2 percentage points by year-end 2026 relative to our baseline forecast, obtained from the Blue Chip Economic Indicators in January 2026.

The reduction in average tariffs assumes that no further changes in trade policies are expected. However, since the court ruling, the United States Trade Representative has started multiple tariff investigations—most prominently, those into Section 301 of the Trade Act of 1974. Section 301 targets trade practices deemed unfair to U.S. commerce, including theft of intellectual property.

These investigations signal an intention by the administration to introduce additional tariff measures, which could push the average U.S. tariff rate in the 12–13 percent range even after the Supreme Court ruling. Under that scenario, the disinflationary effect of the ruling is damped, and the decline in core PCE inflation relative to the baseline narrows to roughly 0.1 percentage points by year-end 2026.

The takeaway is that the court ruling's effect on inflation is real but modest, and its ultimate size depends on whether replacement tariffs are imposed.

Strait’s closure, higher shipping costs affect U.S.

The Strait of Hormuz is a critical maritime choke point for world trade. While its relevance for trade flows of petroleum products is well known—about one quarter of the volume of crude oil and derived products flow through the strait—a significant volume of chemicals, containers and dry bulk is also transported.

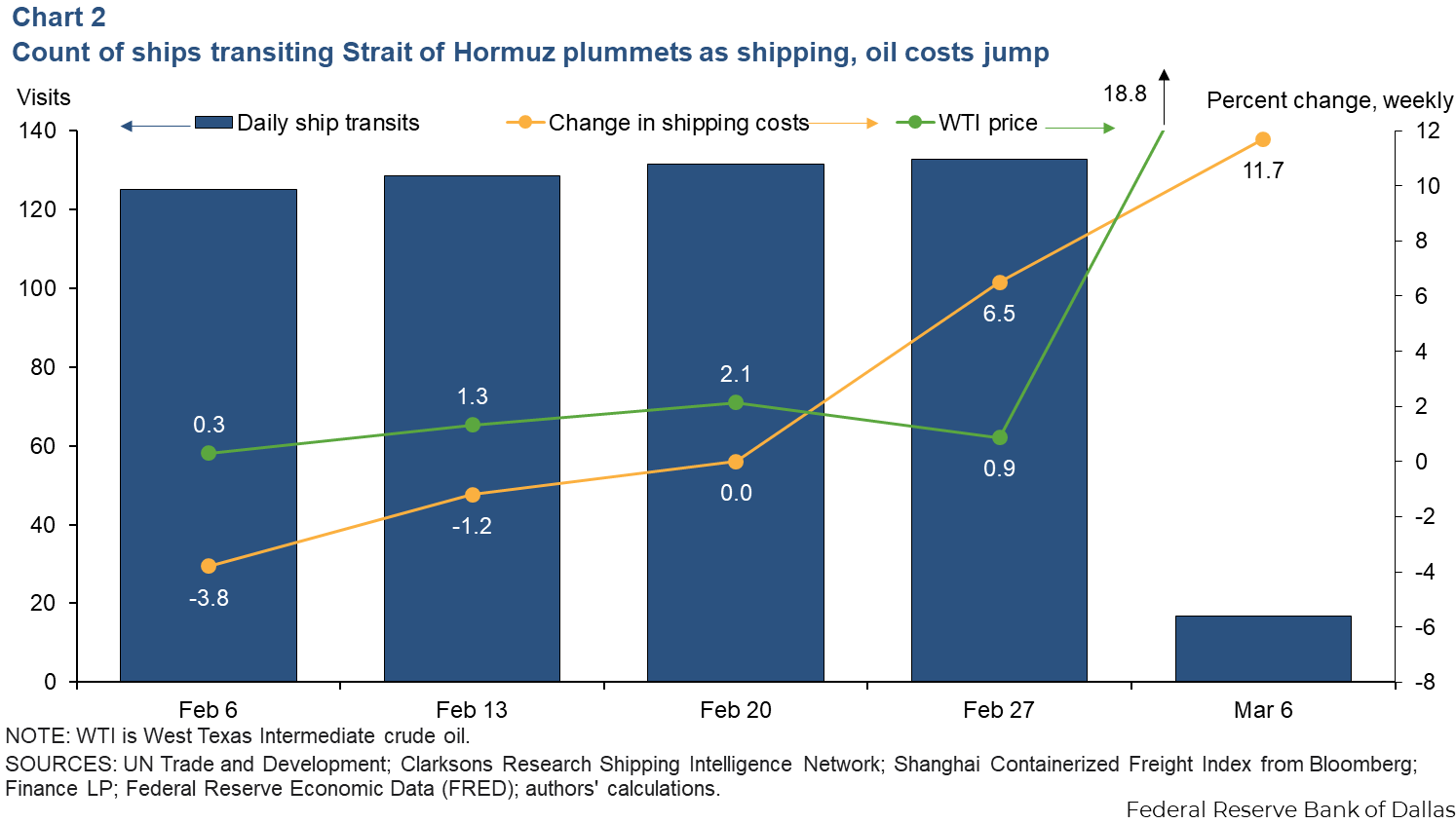

Most importantly, Iran’s closure of the strait led to a near-complete halt of ships transiting beginning March 1, 2026. Hence, even if a small share of non-petroleum products flowed through the strait before the closure, these flows came to a standstill after. Vessels stranded in the Persian Gulf disrupted global shipping logistics. Thus, the strait closure and subsequent disruption led to increased global trade costs, resulting in higher U.S. import costs. The rise counteracted the disinflationary shock generated by the tariff ruling.

In the model, we incorporate an increase in route-specific shipping costs in first quarter 2026 arising from the strait closure. More specifically, we assume that the closure raises the cost of trading intermediate inputs between the Rest of the World bloc (which includes the Middle East) and the other four regions: the United States, China, advanced foreign economies and Asia (excluding China).

We consider a 5 percent trade cost increase, with a persistence that is in line with both historical increases in these costs as well as recent research on the macroeconomic effects of supply chain shocks. Although shipping costs increased significantly more than 5 percent after closure of the strait, we consider 5 percent as a reasonable benchmark reflecting the conflict-related shipping costs increase, but independent of the succeeding oil price rise.

By comparison, the Shanghai Containerized Freight Index increased more than 50 percent between Feb. 20 and April 10. Specifically, it jumped more than 6 percent during Feb. 20–27, just before the drop in ship transit through the strait and the surge in oil prices (Chart 2).

We interpret the freight index increase as generated by disruptions in global shipping—likely by a spike in Iranian oil exports and shipping insurance premiums immediately before the closure—independent of the large increase in oil prices that followed. Hence, we see the 5-percent trade cost increase in the model as a lower bound on the actual amount since the closure of the strait.

Hormuz closure impact exceeds tariff ruling disinflationary impact

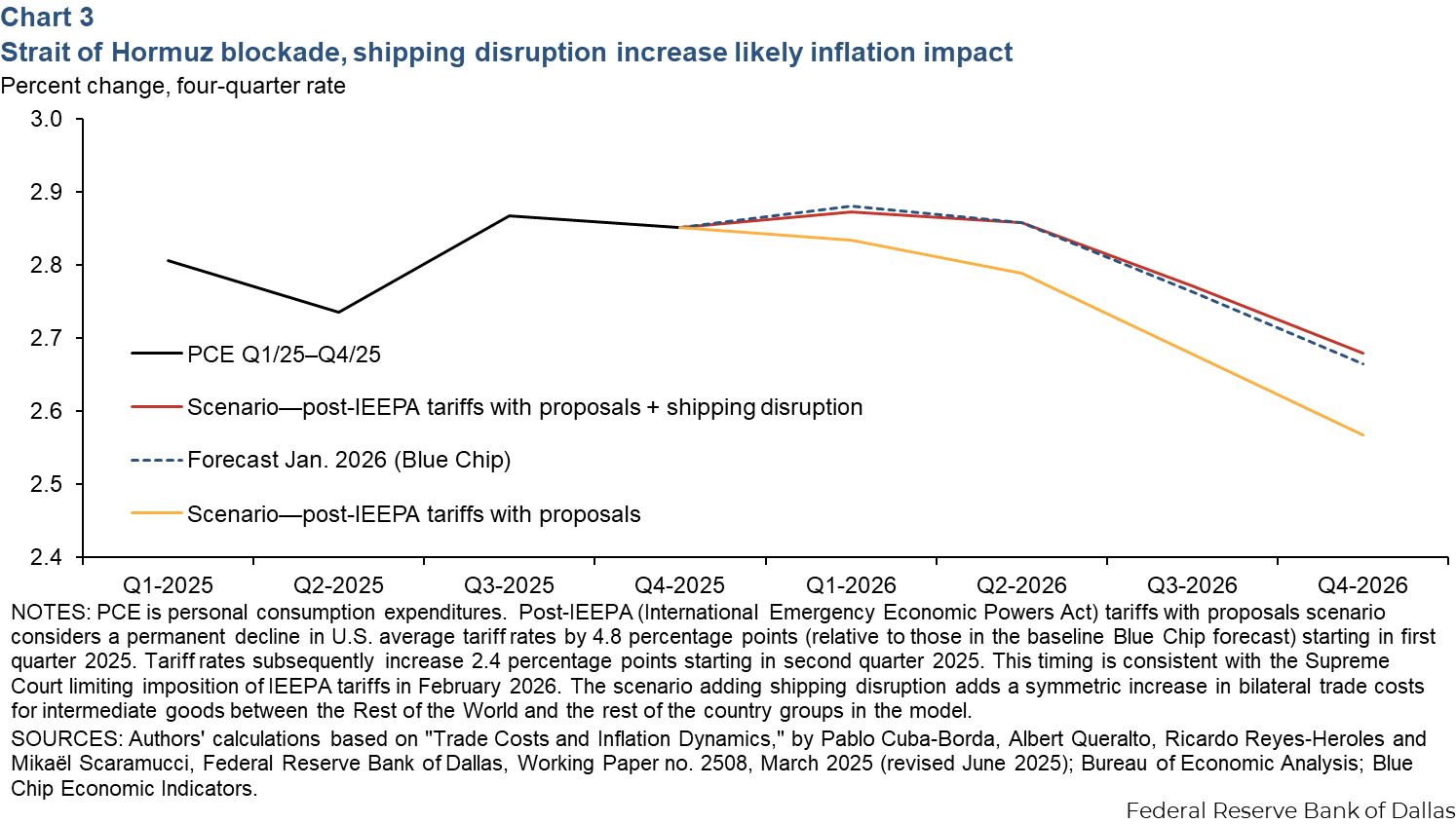

Chart 3 plots the model-generated core PCE inflation in the U.S. that emerges from adding the shipping-cost shock to the post-Supreme Court ruling tariff change.

The inflationary effects of the blockade entirely offset the disinflationary impact of the expected lower post-IEEPA tariffs through year-end 2026. This adds approximately 0.1 percentage points to four-quarter core PCE inflation in the final quarter of 2026.

The shock works through two channels. The first is by directly raising the cost of importing intermediate inputs to U.S. producers. The second channel works indirectly, by raising the cost of intermediates traded among major U.S. trading partners, which then feeds back into U.S. import prices.

The combined effect builds gradually as higher input costs work their way through production chains, which is why the inflation impact is most visible in the final quarter of 2026, rather than at the time of the shock.

Strait closure mitigates court’s tariff ruling

Our analysis suggests that post-IEEPA expected tariff reduction would, in isolation, lower core PCE inflation by roughly 0.1 percentage points by year-end 2026. The increase in shipping costs associated with the Hormuz blockade will, however, completely offset these disinflationary effects over the same horizon, leaving the net effect on inflation through 2026 close to zero.

Even though substantial uncertainty surrounds the assumption underlying our analysis, we consider the 5 percent increase in shipping costs a strict lower bound on the actual increase in international trade costs triggered by the closure. As a result, deepening inflationary pressures arising from the disruptions in the global shipping environment should be expected.

About the authors

Ricardo Reyes-Heroles is a principal research economist in the Research Department at the Federal Reserve Bank of Dallas.

Tryg Aanenson is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.