Texas multifamily housing yet to stabilize; downside risks remain

A pandemic-era surge in multifamily construction created an oversupply nationally and in many Texas markets. Vacancy rates rose; rents fell.

Since peaking in mid-2024, vacancy rates have improved. Meanwhile, rents are still declining in most Texas metro areas. Concessions remain widespread, pressuring valuations of new construction and older properties.

Texas banks’ double-digit loan growth supported the increase in multifamily supply during a period of strong housing demand and low financing costs. Historically, bank lending for multifamily housing has been characterized by low delinquency and charge-off rates.

Still, the sector has experienced periods of stress, including the early 1990s and during the Global Financial Crisis in the late 2000s, when delinquency rates rose. The current situation points to some potential downside risks.

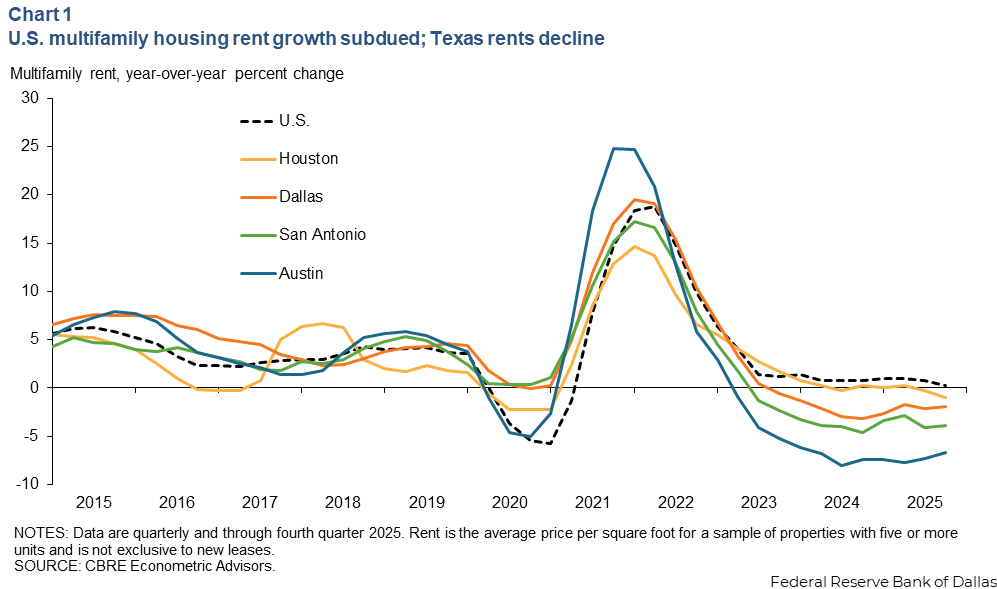

Texas multifamily rents still falling

Rent growth remains subdued nationwide. Rents have declined across Texas due to excess rental property supply (Chart 1). The sharpest rent drops in the state have been in Austin, San Antonio and Dallas.

Landlord concessions are widespread, ranging from six to eight weeks of free rent to as much as 10 to 12 weeks in some Texas submarkets. The share of apartment properties offering concessions is more widespread in Texas major metro areas relative to the nation (Chart 2). Austin leads the Texas major metros in rent concessions followed by Dallas. Concessions are expected to continue through mid-2026, restraining rent growth despite healthy demand fundamentals.

Priced-out homebuyers support multifamily demand

Population growth, which accelerated in the postpandemic period, has supported apartment demand in Texas along with persistent affordability challenges in the single-family housing market.

Households have delayed homeownership, as elevated home prices and mortgage rates make buying unaffordable for many. The U.S. homeownership rate among people under age 35 has dipped from just above 40 percent in early 2000 to 37.9 percent in fourth quarter 2025, according to the Census Bureau.

In the 35-44 age range, the homeownership rate has stabilized at 61 percent following earlier declines. Affordability challenges are steering young adults and millennials toward renting versus owning a home, supporting apartment demand.

Excess supply still plagues rental markets

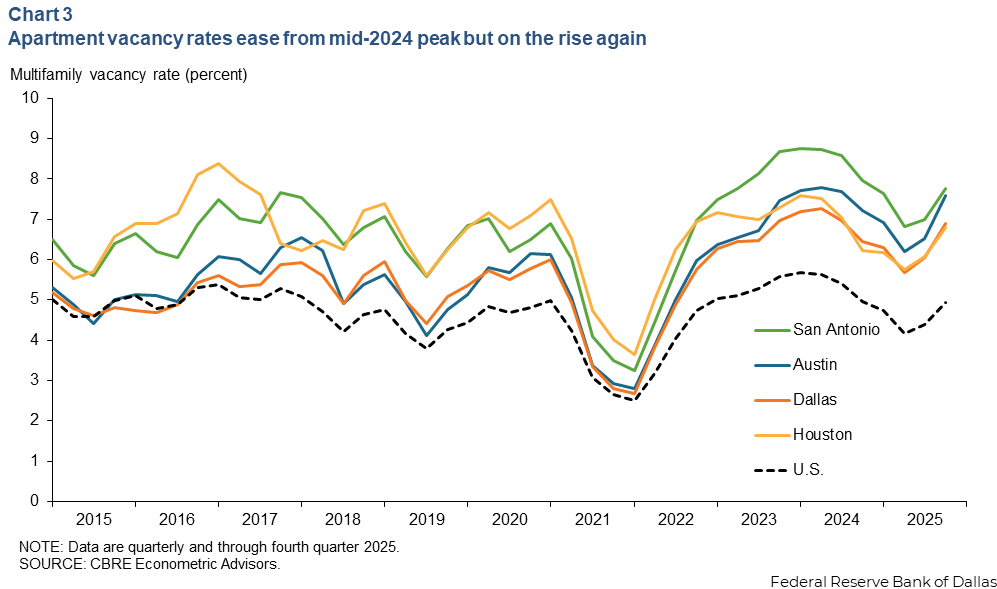

Simultaneously, oversupply continues to weigh on vacancies, particularly in Texas and other Sun Belt markets that experienced a wave of new building in the wake of the pandemic. Demand (net absorption), while solid, lagged supply growth leading to rising vacancy rates (Chart 3).

While vacancy rates are down from their mid-2024 highs as landlords prioritized occupancy over rents, the improvement is a product of increased concessions, flexible lease terms and more competitive pricing. Some of the oversupply consists of luxury, high-priced apartments. It is less clear how much demand exists for these units at market prices (without concessions).

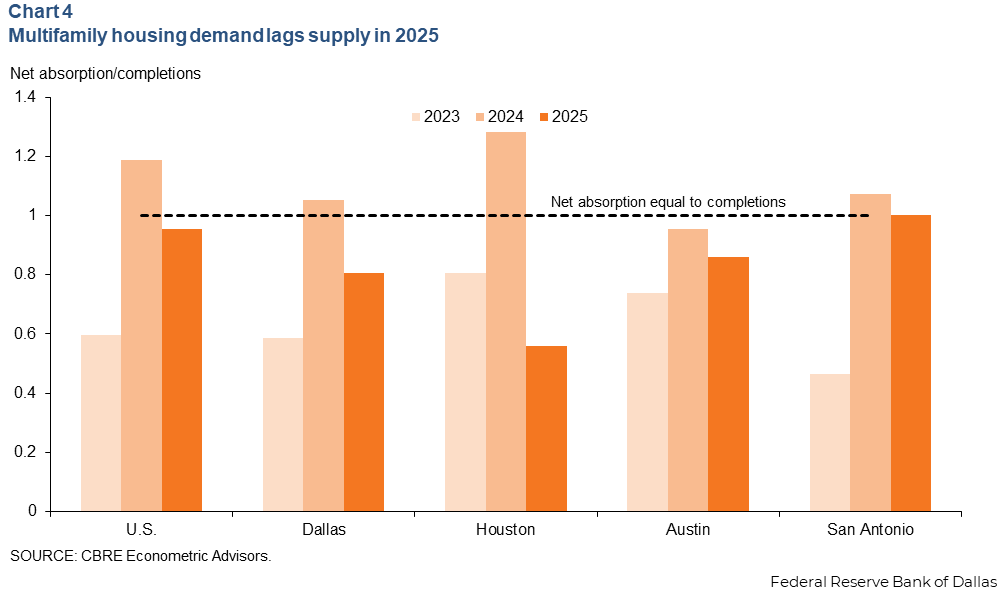

The supply wave is easing. After a pandemic surge, multifamily construction permits have declined across Texas major metro areas and are slightly above prepandemic levels. However, multifamily housing demand has also slowed, with net absorption lagging completions both nationwide and in most major Texas metros in 2025 (Chart 4).

Apartment market fundamentals should improve as deliveries of new buildings decline this year. However, progress will be uneven. Texas markets face lingering headwinds from elevated supply and continued discounting pressure.

Areas with slower population and job growth are likely to also take longer to rebalance, while supply constrained metros will see faster normalization. Thus, apartment managers may continue to emphasize operational efficiency and tenant retention, even as broader fundamentals gradually strengthen.

Bank financing supports multifamily building spurt

Multifamily construction relies on debt financing, which typically accounts for 60–70 percent of the overall financing for a new building. Project sponsors provide the remaining funds in the form of equity.

Bank loans are typically structured to pay interest only during the two-to three-year construction period. As the property is leased toward the end of the construction loan term, the sponsors typically secure long-term financing that will pay principal and interest over a 20-to 30-year amortization period. The proceeds from this long-term financing are used to repay the construction loan.

The pandemic prompted a multifamily construction boom, especially in Texas, as people moved in from big-city coastal markets to more affordable areas where they could work from home. The increased demand for housing, along with low interest rates and a struggling office market, made multifamily housing the favored asset class for banks. Since 2021, multifamily loans have been the fastest growing loan category at Texas banks, with annual double-digit growth rates as banks helped finance the wave of construction.

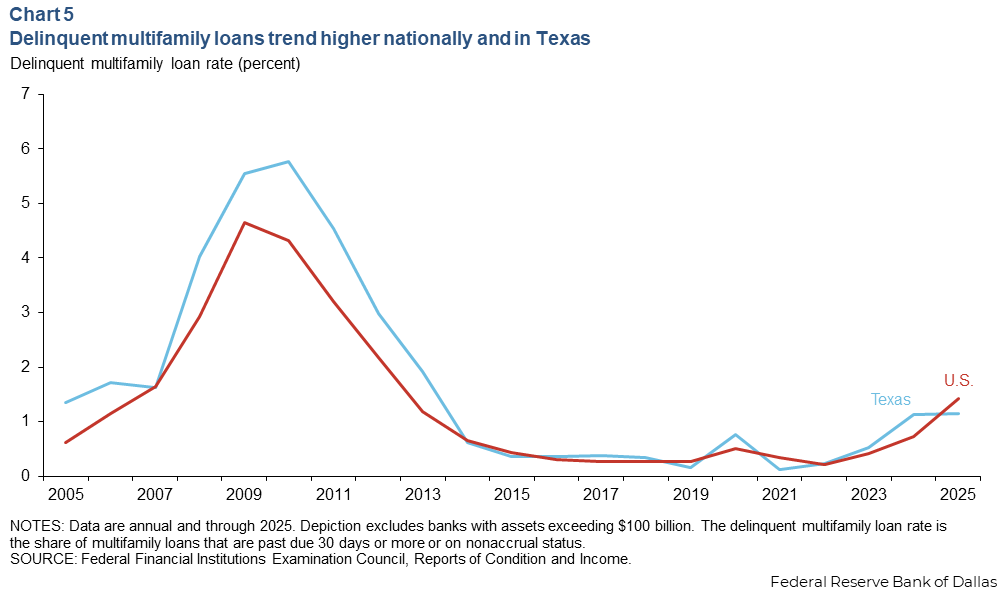

Multifamily loan performance slipping

Delinquency rates for multifamily loans have ticked up but remain low by historical standards (Chart 5). Nonetheless, the recent increase bears watching, as it could present financial risk to some banks. Several factors appear to be contributing to the uptick in delinquencies.

Declining rents and higher-than-normal vacancy rates are headwinds to project net operating income and property valuations. In some cases, the multifamily property’s net operating income is insufficient to service the required interest-only payments, and the project sponsor will cover the shortfall—contributing more equity—to ensure the loan does not become delinquent.

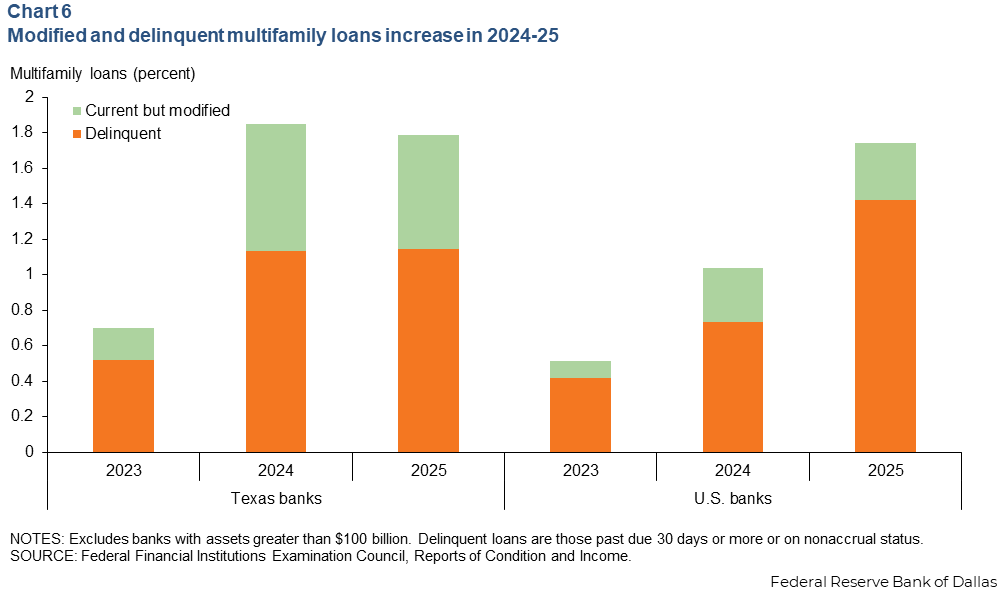

Insufficient net operating income also makes it difficult for some multifamily properties to obtain long-term financing. Under certain circumstances, banks can modify loan terms for borrowers experiencing financial difficulties. These modifications have increased for multifamily loans (Chart 6).

For Texas, with its elevated multifamily housing supply, the share of modified multifamily loans exceeds the U.S. overall. Some banks have modified loan terms, extending maturities and hoping that additional time will result in higher occupancy levels and increased net operating income. Most of the recent multifamily loan modifications are current on scheduled loan payments.

Where project sponsors decline to cover cash flow shortfalls, the loan could become delinquent. Later, as the loan maturity date approaches, a property may fail to secure long-term financing. Subsequently, if a property were sold in liquidation, it could fail to attract offers at least equaling the construction loan amount, possibly requiring a bank loan charge-off. When a multifamily loan is in default, the parties bearing a financial loss could include the equity sponsor, third-party guarantors backing the loan, the bank, or a combination of these parties.

During the Global Financial Crisis, the unemployment rate was strongly correlated with multifamily loan performance. As people lost their jobs and primary sources of income, paying rent and other living expenses became more challenging. Both the unemployment rate and the multifamily loan delinquency rate have ticked up in recent years. If the unemployment rate markedly increases, reflecting a deterioration in the labor market, the multifamily sector could experience additional downward pressure.

Bank multifamily loan concentrations appear manageable

Most Texas banks do not appear to have elevated multifamily loan concentrations—only a few report multifamily loans in excess of capital and loan loss reserves. In addition, none of the bankers surveyed for the Federal Reserve Bank of Dallas’ Banking Conditions Survey in November 2025 selected “extremely concerned” about the performance of multifamily loans. As with most forms of real estate, the performance of multifamily loans will vary by factors that include property specifics, location and sponsor. If banks were to experience problems with multifamily loans, the issues would likely be idiosyncratic to specific borrowers in loan portfolios.

While market factors appear to be stabilizing in the multifamily sector, some risks remain notable. A fair amount of excess supply remains in some markets, and new properties are facing longer lease-up timelines.

Still, various market researchers project a gradual resumption of rent growth in late 2026 and 2027, driven by moderating new unit deliveries and solid consumer demand.

About the authors

Laila Assanie is a senior business economist in the Research Department of the Federal Reserve Bank of Dallas.

Lorenzo Garza is a vice president in Banking Supervision at the Federal Reserve Bank of Dallas, where he oversees teams responsible for supervisory risk, policy and bank surveillance.

Kelly Klemme is a lead data scientist in the supervisory risk, policy and surveillance division of the Banking Supervision Department at the Federal Reserve Bank of Dallas.