COVID-19 exposes mortgage market vulnerabilities that led to volatility, Fed intervention

The COVID-19-induced financial market shock in March 2020 significantly disrupted the market for agency mortgage-backed securities (MBS)—those guaranteed by Fannie Mae (Federal National Mortgage Association), Freddie Mac (Federal Home Loan Mortgage Corp.) and Ginnie Mae (Government National Mortgage Association).

Mortgage real estate investment trusts (MREITs), which invest in mortgage loans and securities backed by residential and commercial properties, are viewed as the marginal investors in the agency MBS market. MREITs principally finance these holdings with short-term debt and became deeply affected by the COVID-19 shock. To quickly generate liquidity, they sold agency MBS—a deleveraging that contributed to market volatility.

The Federal Reserve responded to these dynamics by purchasing agency MBS and, for the first time, agency commercial mortgage-backed securities (CMBS). Lessons learned a decade earlier during the global financial crisis about the adverse effects of dysfunction in core asset markets proved instructive in the Fed response.

Mortgage REIT investment activities

Real estate investment trusts (REITs) are specialized investment vehicles that by law must hold and derive most of their income from real estate-related assets. They are exempt from federal corporate income tax if they distribute to their investors at least 90 percent of their taxable net income annually. REITs generally specialize in either owning real estate assets or providing debt financing for them.

We will focus on MREITs, of which there are two broad classes. Agency MREITs predominantly invest in mortgage-backed securities implicitly or explicitly guaranteed by the U.S. government—with timely principal and interest payments guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae.

Hybrid MREITs invest in a wider array of fixed-income assets secured by real estate. They include securities such as agency MBS and CMBS, privately issued MBS and CMBS, credit risk transfer securities (Fannie Mae and Freddie Mac general obligation debt without implicit repayment backing), and residential and commercial real estate loans. While agency MBS are widely traded among investors, the other asset classes are much less liquid.

MREITs finance MBS holdings using repurchase agreements

There were 39 MREITs with combined assets of $681 billion at the end of 2019. Together these entities held $335 billion of agency MBS (49 percent of total assets) and financed themselves predominantly using repurchase agreements ($380 billion, or 56 percent of total assets). “Repos” are short-term secured borrowing agreements in which parties agree to sell and repurchase assets at set times and prices.

MREITs’ agency MBS holdings are largely financed by broker-dealers using repurchase agreements. A characteristic of these arrangements is the collateral “haircut” establishing the share of debt that can be incurred against the value of an underlying asset.

These assets are not subject to credit risk due to the guarantees provided by the respective federal agencies. However, this trading strategy creates interest rate and liquidity risk, which MREITs primarily mitigate using interest rate swaps—a transaction among parties involving a fixed-rate return in exchange for a variable-rate return over a set period.

Impact of large-scale MBS purchases

A recent Dallas Fed working paper explores the relationship between the Federal Reserve’s large-scale purchases of agency MBS after the global financial crisis and the MREITs’ management of their agency MBS portfolios. Of note was the dramatic expansion in MREIT holdings—especially involving agency MREITs—after the Fed’s first round of quantitative easing. The period covered ran from December 2008 to March 2010, when the central bank injected cash into the financial system by purchasing Treasury securities and agency MBS.

This development caught the attention of the federal Financial Stability Oversight Council in 2013. The panel, created in the aftermath of the global financial crisis, expressed concern about the vulnerability of these MREITs to sharp interest rate increases that would erode the value of their assets. A characteristic of bonds and debt instruments is that their value moves inversely to interest rates—rising rates depress the market value of debt.

Regulators worried about a run on MREITs’ short-term liabilities and a large-scale selloff in the agency MBS market as rates rose. The council’s insights were prescient.

Effect of the COVID-19 shock on MREITs

The onset of the COVID-19 crisis brought a rapid repricing of risk and a dash for liquidity in financial markets. Market participants, including money managers facing client redemptions, used the relative liquidity of Treasury and agency MBS markets to raise cash as the outlook deteriorated.

Additionally, broker-dealers handling the transactions were limited in their ability to absorb asset sales, owing to balance sheet constraints and tighter risk limits for traders working remotely. The Federal Reserve’s November 2020 Financial Stability Report provides a retrospective of these events.

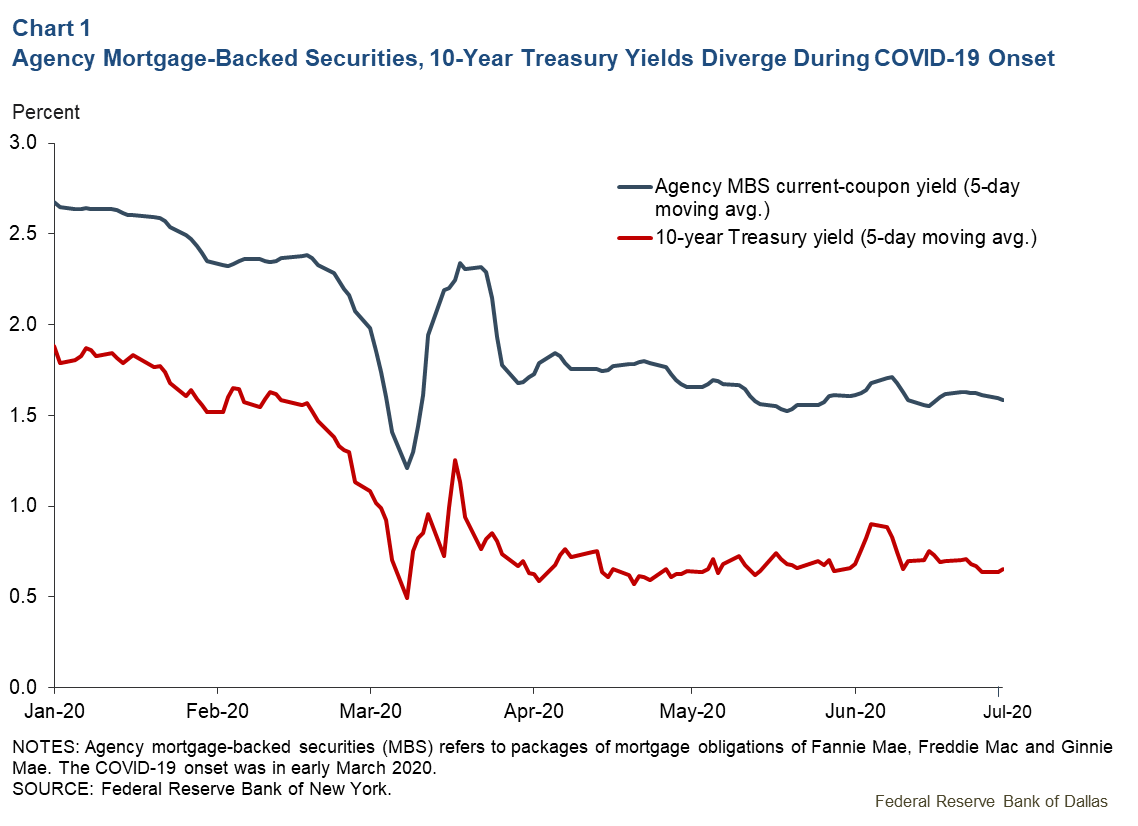

To get a better sense of how market volatility disrupted MREITs, Chart 1 presents five-day moving averages of 10-year Treasury and current-coupon agency MBS yields.

Both series drifted steadily downward during the first two months of 2020, with the agency MBS–Treasury spread remaining relatively stable at around 85 basis points, or 0.85 percentage points.

During the first week of March, however, the 10-year Treasury yield plummeted and agency MBS spreads to that benchmark compressed significantly as a result of the pandemic-related flight to financial safety. But soon after, yields sharply reverted due to investor liquidity demands and dealer balance sheet constraints, with the MBS–Treasury basis widening further due to a sharp increase in interest rate volatility.

Amid the declining liquidity in agency MBS markets and a widening MBS–Treasury spread, many MREITs faced increased margin requirements on their repo-based financing—they needed additional collateral to back their outstanding debt.

To raise cash, these institutions further sold into the already liquidity-challenged market, creating a feedback loop between the widening MBS–Treasury spread and forced deleveraging. Ultimately, MREIT balance sheets collectively contracted by $158 billion during the first quarter, or 23 percent from year-end 2019. Most of the decline came from shedding $124 billion in agency MBS, with repo financing declining in roughly equal measure. Not surprisingly, MREIT equity values fell sharply during first quarter 2020 and finished down over 50 percent on a weighted-average basis.

Federal Reserve responds, adds to MBS holdings

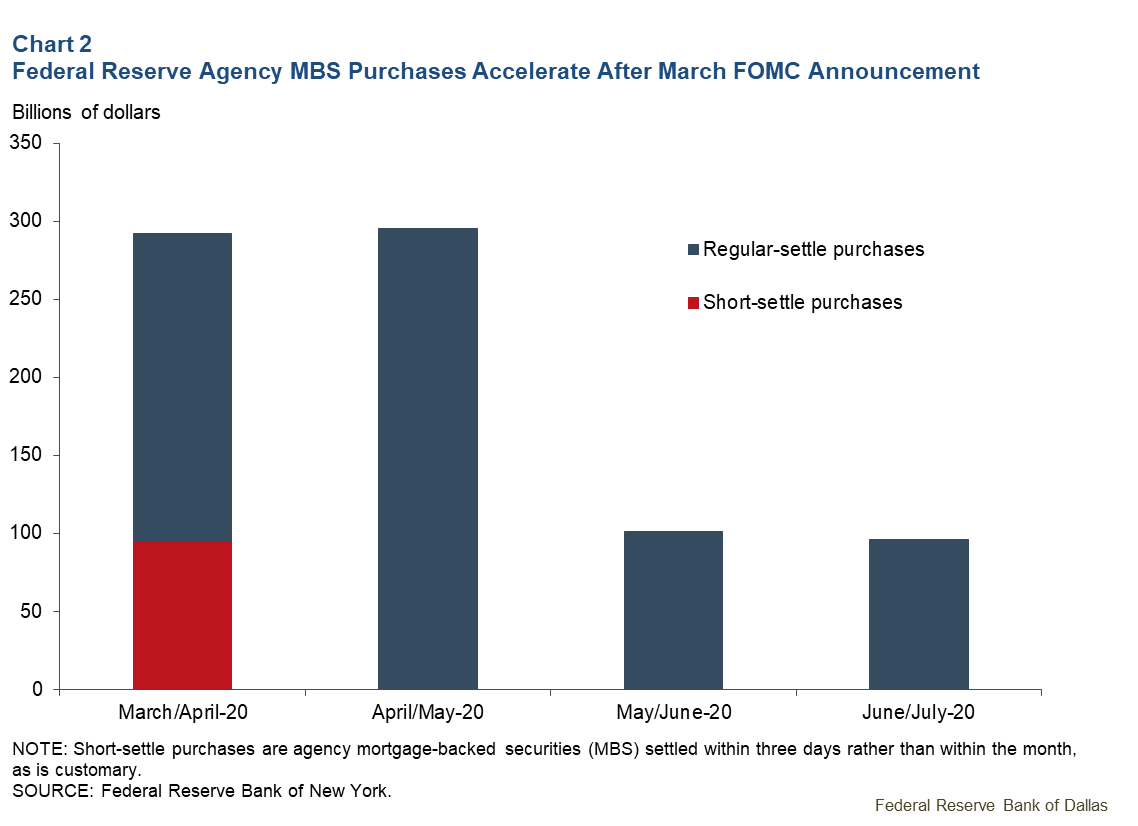

On March 15, 2020, the Federal Open Market Committee announced an increase in agency MBS holdings by at least $200 billion over several months, plus reinvestments, to improve market functioning. At the time of the announcement, the Federal Reserve held just shy of $1.37 trillion in agency MBS; by the end of May, the total had swelled 34 percent to $1.84 trillion. In June 2020, the Federal Reserve modified its approach and started purchasing $40 billion per month of agency MBS, plus reinvestments.

The central bank purchased almost $600 billion of agency MBS as it expanded its holdings and reinvested prepaid principal from March through April (Chart 2).

Of special note was the use of “short settle” transactions during the depths of the March turmoil. The central bank has historically purchased agency MBS in the to-be-announced forward market, where settlement occurs once per month per class of security. However, with the nearest settlement date a month away and market conditions deteriorating, the central bank contracted with its primary dealers—24 large counterparties—to purchase securities and settle within two to three days.

These short-settle purchases helped MREITs and other market participants deleverage while the balance sheet capacity of broker-dealers was constrained.

Working toward a more stable mortgage market

The Federal Reserve’s agency MBS purchases played an important role in mortgage market stabilization in 2020. But the effects on the MREITs have been longer lasting. While the size and valuation of the sector has stabilized, the experiences of these entities have varied depending on their asset composition, funding model, leverage and counterparties.

As result, some MREITs have revisited their business strategies and risk management. Those unable to meet margin calls entered forbearance agreements in March and April and have since negotiated workouts with creditors.

Aftereffects of COVID-19 market turbulence

The onset of the COVID-19 pandemic caused significant dislocations within financial markets, including those for agency MBS. MREITs represent a group of nonbank financial institutions that were deeply affected by—and contributed to—the price volatility in that market.

Federal Reserve asset purchases were a stabilizing force. The Financial Stability Board, an international panel of national financial overseers, has announced that it will soon embark on a holistic review of nonbank financial institutions’ role in causing liquidity imbalances and propagating market stress.

About the Authors

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.