Texas economic growth outpaces nation despite persistent downside risks

Texas employment growth advanced in May, continuing to surpass the national average. Meanwhile, price and wage pressures remain elevated, according to the Texas Business Outlook Surveys (TBOS). Employment growth is projected to slow later this year, while price and wage pressures are expected to ease following Federal Reserve monetary policy tightening.

Manufacturing new orders continued to slide in May, and overall business sentiment and outlooks were negative, TBOS respondents indicated. With high interest rates and tighter credit conditions, risks to the outlook are to the downside.

Employment growth accelerates in May

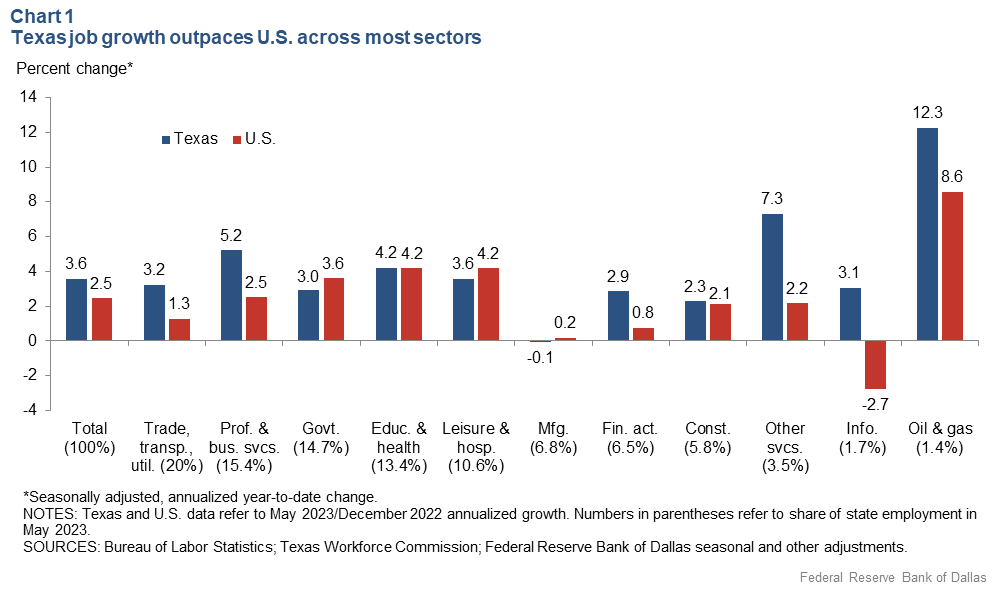

Job growth strengthened in May as the Texas economy added 41,000 jobs—a 3.6 percent annual growth rate, which exceeded the 2.6 percent U.S. rate. April job gains were revised down to 2.5 percent from 2.8 percent.

Employment within manufacturing and leisure and hospitality contracted in May, while every other sector expanded.

With the job growth acceleration in May, Texas has added 201,700 jobs year to date—an annual growth rate of 3.6 percent, which exceeds the nation’s 2.5 percent rate. Texas’ growth advantage over the nation extends to a majority of supersectors (Chart 1).

The state’s services sector has led employment growth in 2023, with professional and business services gaining 44,900 jobs and education and health services adding 31,800 positions. Overall, the services sector has added 186,000 jobs year to date, a 3.9 percent annualized expansion rate. Employment growth notably slowed in interest-rate-sensitive sectors, such as manufacturing, financial activities and construction.

Abating price pressures noted

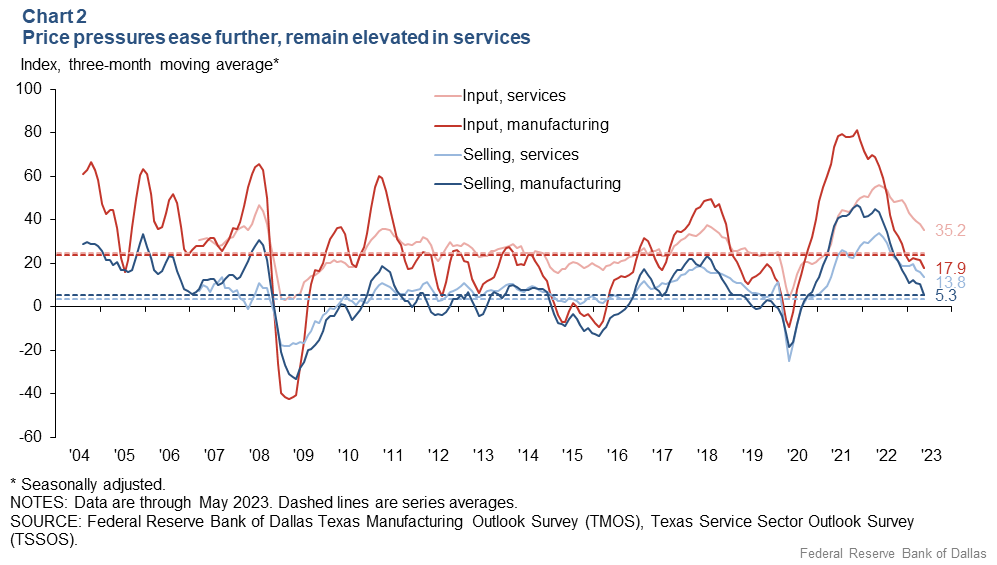

Price pressures remained elevated, though there has been a deceleration during the past year, TBOS respondents said (Chart 2).

Price pressures in manufacturing have declined faster than in services, due in part to slowing demand, firms clearing out backlogs and input costs leveling out as supply chains normalize. The manufacturing selling price index fell below its long-term average in May for the first time in two-and-a-half years, while the input price index remained below average for a fifth consecutive month.

Service sector price pressures, however, remained elevated.

The primary drivers of price increases across the board are higher input and labor costs, with 4 out of 5 firms responding to TBOS special questions in May identifying input or labor costs as a main contributor. Other factors cited included higher demand, lower productivity, and higher taxes and regulation.

Wage growth slowing but still elevated

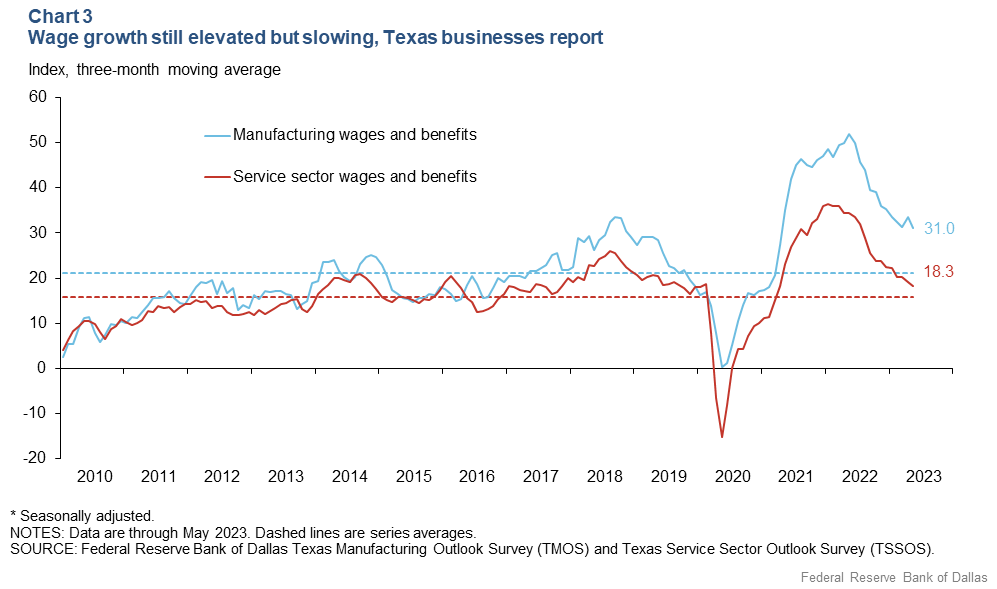

TBOS measures of wage inflation remained above their historical averages in May, although they declined substantially since peaking a little over a year ago (Chart 3).

Manufacturing firms reported greater wage pressures than service sector firms despite flat production in recent months. Manufacturing contacts noted difficulty finding qualified workers since they are competing with other industries that can offer hybrid work and other flexible work arrangements.

Wage growth remains a concern as reflected in TBOS respondents’ comments. One food services firm reported that “hiring remains ridiculously difficult, and upward wage pressure continues unabated.” A professional services firm noted consumer resistance to cost pass-through, saying, “Pricing in high wage inflation will get pushback from our clients and make us less competitive.”

After unprecedented price increases in 2021–22, 40 percent of companies in May 2023 noted it was harder to pass along costs to consumers than six months earlier compared with 36 percent of firms who responded similarly in November 2022. A higher share of companies in manufacturing are having a harder time pushing through increases to customers, 49 percent, than services firms, 37 percent.

Expected 2023 price, wage growth revised lower in May

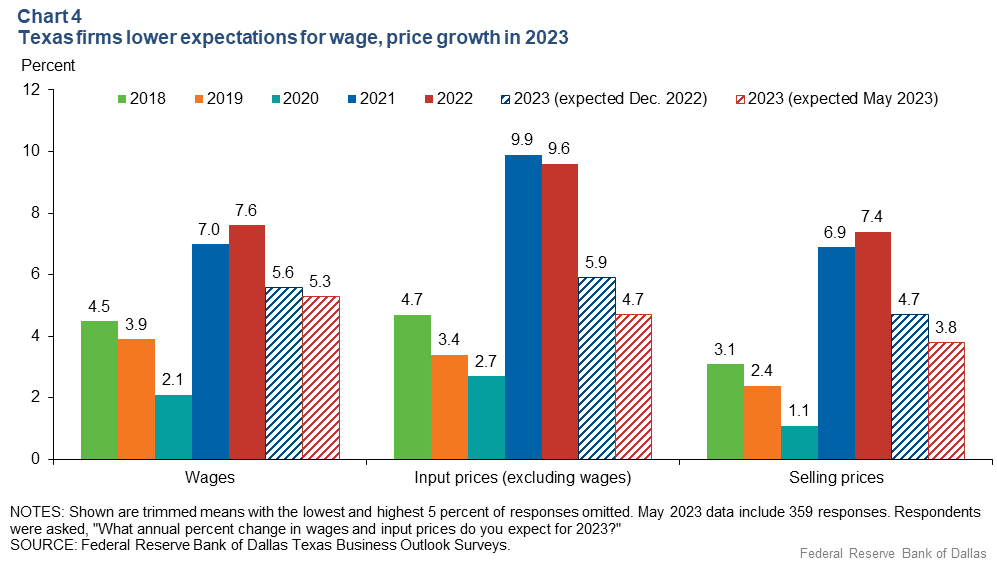

Texas companies expect price pressures to moderate further through year-end. In May, TBOS respondents revised their expectations lower for price and wage growth relative to what they reported in December 2022 (Chart 4).

Firms anticipated a 4.7 percent increase in input prices, a 5.3 percent increase in wages and a 3.8 percent increase in selling prices this year on average. Though wage growth is expected to moderate from 2022 levels, the revision to anticipated wage growth between December and May was notably smaller than the expected changes for input and selling price increases.

Input price expectations for 2023 are now even with actual input price inflation that TBOS respondents experienced in 2018. Wage and selling price growth both remain above prepandemic levels.

Fed interest rate policy may weigh on Texas growth

The Federal Reserve’s actions to curb inflation through interest rate increases are expected to contribute to slower economic growth, though Texas will likely continue to outperform the nation. The state’s faster pace reflects historically greater economic growth and labor force expansion. Additionally, the state’s labor markets are more efficient, with Texas workers more likely to find suitable jobs and Texas firms more easily attracting qualified workers than their counterparts nationally.

However, the latest Dallas Fed Texas Employment Forecast anticipates 2.8 percent employment growth in Texas in 2023, implying a job growth slowdown to an annualized rate of 2.2 percent for the rest of the year. December-over-December growth would thus be above the long-term trend growth of around 2 percent for the state but weaker than the 4.1 percent expansion in 2022 and the 6.1 percent rate in 2021.

Overall business sentiment and outlook indexes have also been negative, suggesting possible weakness ahead.

TBOS comments illustrate a lack of clarity surrounding the outlooks. One manufacturer noted, “Business is slowing down. That is certain.” Meanwhile, a services firm said, “Despite talk of recession and economic downturn, there is no apparent evidence of such.”

About the authors

Anil Kumar is an economic policy advisor and senior business economist in the Research Department at the Federal Reserve Bank of Dallas.

Ana Pranger is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.