Service sector leads Texas gains; firms say credit constraints not binding

Texas economic activity expanded at a modest pace in May, driven by the service sector. Texas employment growth picked up, and the unemployment rate nudged up to 4.0 percent in April from 3.9 percent in March.

Inflation continued to decline, and wage growth remained stable. However, both were elevated compared with prepandemic rates. Dallas Fed Texas Business Outlook Surveys in May indicated that fewer Texas businesses are seeking credit, with many saying they already have the funds necessary to meet their needs. Additionally, fewer businesses reported difficulty obtaining credit.

Texas economic activity ticks higher

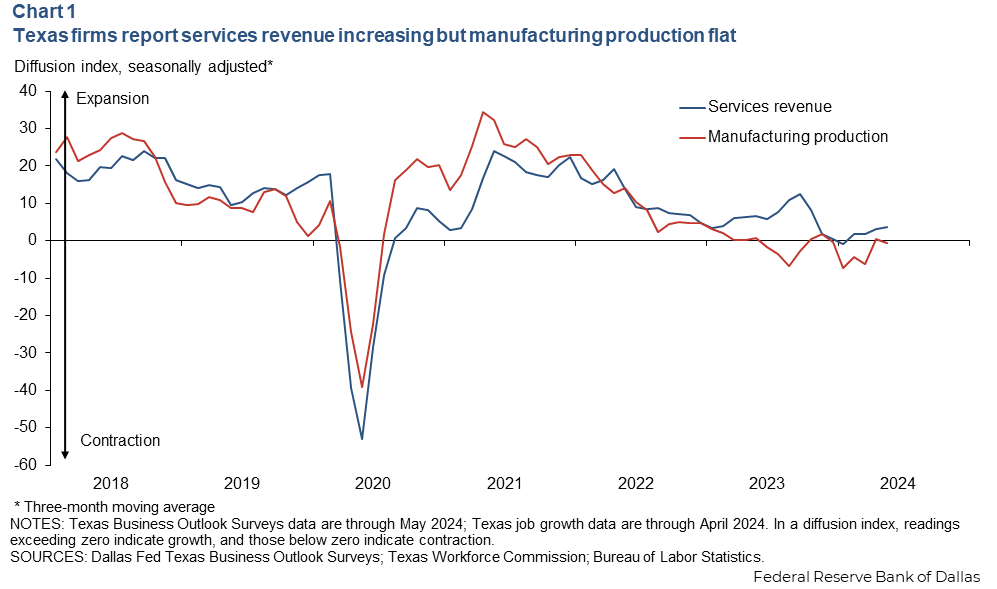

The three-month moving average of the Texas Service Sector Outlook Survey (TSSOS) revenue index continued moving higher in May, suggesting acceleration of service sector activity, though growth remains at a below-average pace (Chart 1).

Meanwhile, the Texas Manufacturing Outlook Survey (TMOS) production index signaled flat activity in the manufacturing sector after declines earlier in the year. Because the service sector accounts for about 86 percent of the economy and revenue increased, these readings indicate the overall economy expanded.

The Texas Business Outlook Surveys are diffusion indexes—the share of firms reporting an increase minus the share of firms reporting a decrease. Positive index values represent expansion, and negative values represent contraction.

Retail sales remained weak in May according to both the Texas Retail Outlook Survey (TROS) and Texas retail sales tax data. Contacts for the Beige Book, an eight-times-a-year qualitative analysis of regional conditions, reported elevated prices were suppressing consumer demand.

Job growth continues

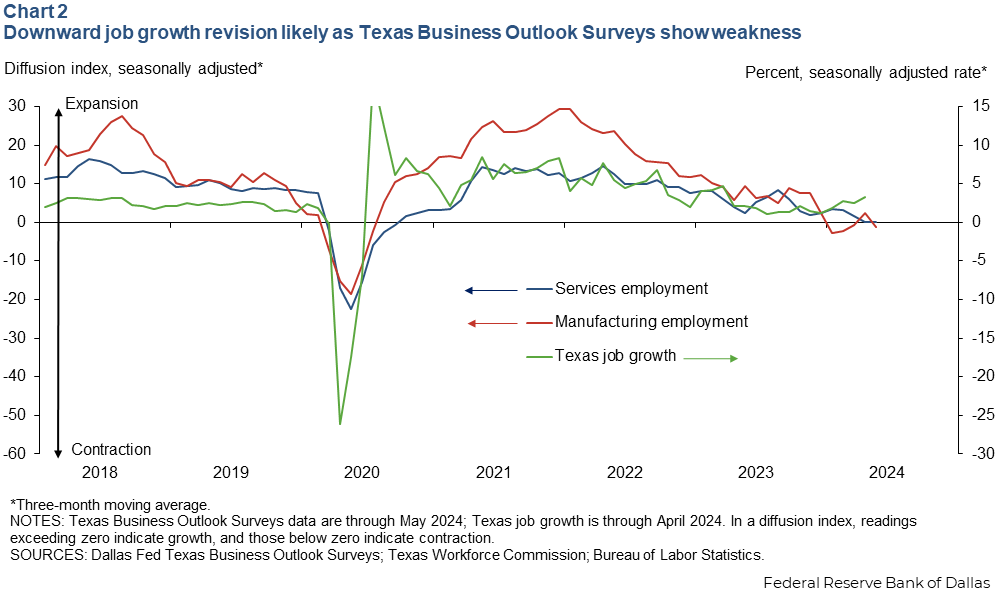

Texas employment data showed payrolls grew an outsized annualized 4.0 percent month over month in April, pushing up 2024 year-to-date growth to 2.9 percent. This represents an acceleration over last year when the number of Texas jobs grew 2.3 percent.

However, recent payroll job gains have been revised down during the benchmarking process—the adjustment of initial survey data to reflect more comprehensive administrative data subsequently available in the Quarterly Census of Employment and Wages (QCEW). Texas payroll employment growth was revised down 1.3 percentage points in the second half of 2023.

Similar downward revisions are expected for U.S. employment data when benchmark revisions are incorporated into the Bureau of Labor Statistics’ January 2025 payroll employment release. In the meantime, the Federal Reserve Bank of Philadelphia publishes earlier estimates of benchmarked U.S. employment data. The bank’s June 13 release resulted in a 1.1-percentage-point downward revision of U.S. job growth for the second half of 2023.

The Texas benchmarking for the first and second quarters of 2024 will not occur until the next QCEW release in fall 2024. Until then, TBOS employment indexes, which have weakened further, provide a clue regarding the direction of upcoming revisions. The three-month moving average of the TSSOS employment diffusion index was zero in April and May, indicating neither expansion nor contraction (Chart 2).

In the second half of 2023, TMOS and TSSOS employment indexes persistently declined, signaling below-average job growth. This occurred despite payroll data showing a pick-up in growth. After downward revisions due to early benchmarking, the payroll data fell closer in line with the TBOS trend.

Inflation falling but remains high

Inflation continued to slow, declining 4 percent year over year in April after reaching 5 percent in December 2023, according to the Texas consumer price index. These drops were driven by disinflation in services, excluding shelter and medical services. Inflation in shelter, a category that includes apartment rent and homeowner’s equivalent housing cost, has remained elevated at around 6 percent since December 2023, and medical services inflation has increased in Texas since the beginning of 2024.

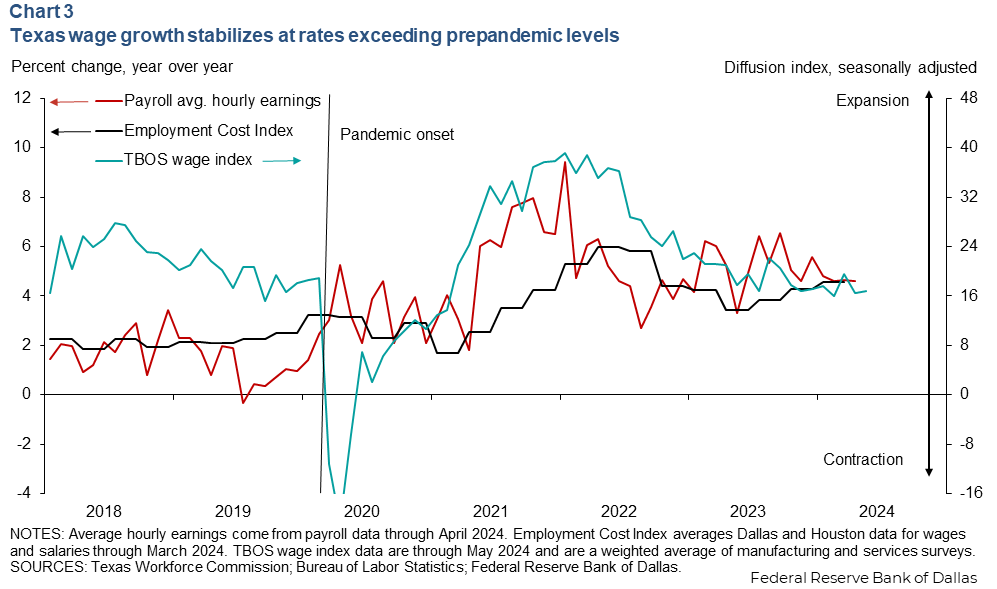

Wage growth has also stayed high but is stabilizing, according to the Employment Cost Index (ECI) data and the payroll survey of average hourly earnings, both from the Bureau of Labor Statistics, and the TBOS wage index (Chart 3).

The TBOS wage diffusion index has approached prepandemic levels, indicating that wage increases no longer occur at the heightened frequency they did coming out of the pandemic. However, both the ECI and the average hourly earnings show wages growing at about 4.5 percent, above prepandemic norms of 2.5 percent.

Forward-looking measures offer a slightly different perspective. As of March, TBOS firms expected wage growth of 3.6 percent on average over the subsequent 12 months. In May, Philadelphia Federal Reserve Bank surveys showed expected wage growth of 3.0 to 3.5 percent for services and manufacturing firms over the coming 12-month period.

Texas firms report not feeling credit constrained

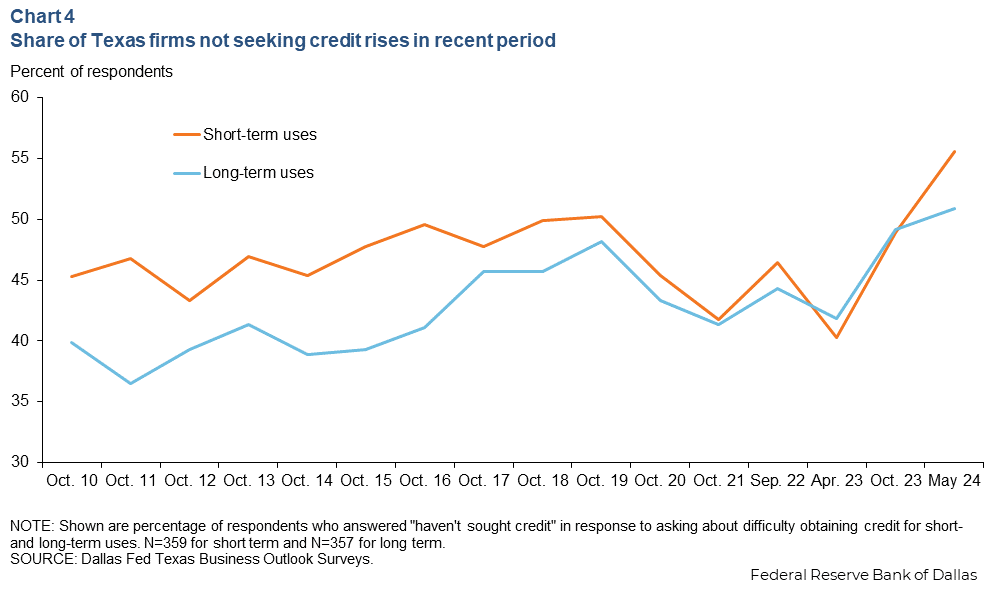

A puzzle for central bankers has been strong economic growth despite higher interest rates. TBOS special questions in May asked firms directly about their demand for and access to credit. A large proportion reported not seeking credit. Among those who sought credit, a smaller share reported difficulty obtaining it relative to the last time the question was asked, in October 2023. In addition, bank loan volume grew slightly after a year of declines, according to the Dallas Fed Banking Conditions Survey in May.

In the May TBOS, 56 percent of Texas businesses reported not seeking credit for short-term uses, such as paying employees, up from 49 percent in October 2023 (Chart 4).

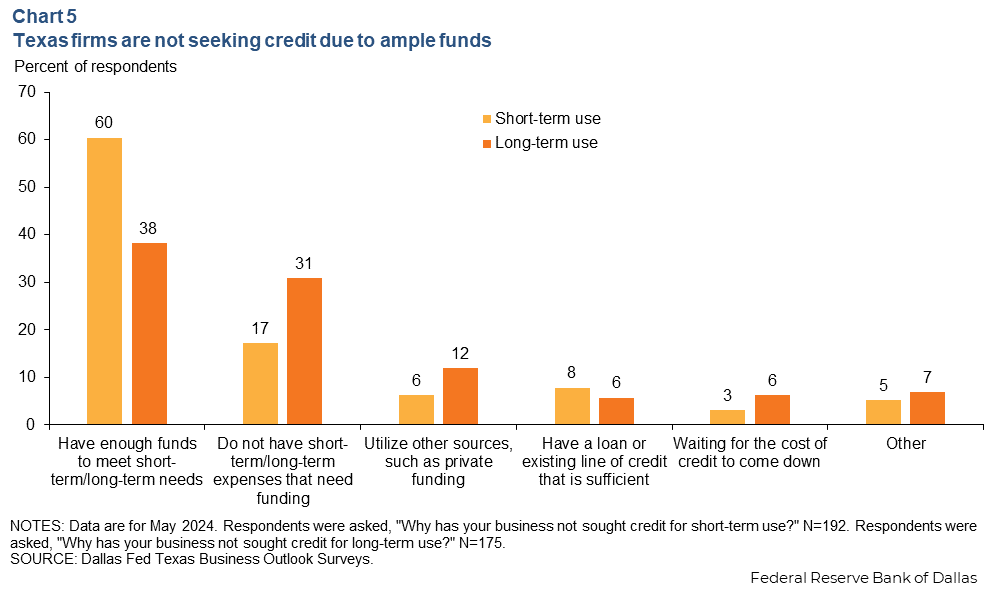

Similarly, half of businesses reported not seeking credit for capital expenditures and other such needs. The high cost of credit was not the reason; only around 5 percent of firms said they were “waiting for rates to drop” before borrowing. Rather, respondents said they have necessary funds in hand and no reason to borrow more, followed by not having expenses that require funding (Chart 5).

Fewer firms cited difficulty obtaining financing relative to October 2023. For short-term uses, firms reported it was less difficult to obtain a loan than in September 2022. One respondent said: “We worked in April and May to increase our credit line by about 30 percent. The bank we have been working with did not have an issue extending more credit to us, as our sales have remained strong this year.”

As Texas businesses are relying on existing funds or having less difficulty obtaining credit, they will not need to curtail activity due to financing issues. As one survey respondent indicated. “We are actually adding people pretty aggressively to grow our company. Most of the time, we sit on $80 million to $100 million in cash.”

The Dallas Fed employment forecast in May showed above-average growth of 2.4 percent for the remainder of the year. Thus, the outlook suggests that economic growth will continue.

About the authors

Mariam Yousuf is a business economist in the Research Department of the Federal Reserve Bank of Dallas.

Isabel Dhillon is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.

Diego Morales-Burnett is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.