Taiwan firms key to nearshoring and reshoring to support AI boom

While China’s trade and investment with Mexico have attracted significant attention, Taiwan firms’ investment in both Mexico and Texas is arguably more significant for the evolution of U.S.–Mexico production networks. Taiwan’s top electronics manufacturers, which play a leading role in advanced manufacturing globally, have been shifting production for advanced IT hardware from China to Mexico and the U.S.

Taiwan firms have been central to U.S. efforts during the past two administrations to reshore critical semiconductor production. The CHIPS and Science Act, signed into law in 2022 during the Biden administration, provided over $40 billion in grants and investment incentives to boost domestic semiconductor manufacturing, research and workforce development.

While modifying the approach, the Trump administration has continued this priority, including through a recently announced U.S.-Taiwan trade deal, calling for $250 billion in investments from Taiwan to expand advanced semiconductor, energy and artificial intelligence-related production in the U.S.

Taiwan’s increasing role in North America as a trade partner and investor is in some ways a mirror image of rising geopolitical tensions with and derisking from China. Taiwan firms were among the first to begin diversification out of China in the 2010s.

With demonstrated success rebuilding complex supply chains in different markets, including Southeast Asia, these firms are well-positioned to support reshoring and nearshoring production of a range of products that may be harder for the U.S. or Mexico to replicate on their own. Notably the U.S.-Taiwan trade deal includes a provision for Taiwan to help the U.S. establish world-class industrial parks in the U.S.

Taiwan’s top contract manufacturers—trendsetters in the electronics industry in previous waves of Mexico’s manufacturing evolution—already play a key role in the rapid U.S. artificial intelligence (AI)-related data center buildout, much of it in Texas. Mexico’s exports of data center equipment to the U.S., particularly from Taiwan-invested firms, have risen rapidly, exceeding $70 billion in 2025. Further production is set to come online in the coming months.

Simultaneously, Taiwan investment in Texas has surged and appears to be at a key inflection point. Leading Taiwan contract manufacturers have announced in recent months their first investments in U.S. manufacturing plants, in particular to produce and assemble advanced servers and equipment for U.S. AI data centers. Overall, Taiwan firms disclosed in 2025 an estimated $5.3 billion in planned foreign direct investment (FDI) in Texas.

Such outlays on both sides of the border are an initial success case of nearshoring a critical supply chain back to North America. In Mexico, Taiwan investment is supporting a shift up the value chain toward more advanced manufacturing, as wage increases have squeezed out lower valued-added operations. In the U.S., Taiwan firms play a central role in rebuilding domestic manufacturing capacity.

Key firms locating large operations on both sides of the border points to potential for the twin plant model originally envisioned in the North American Free Trade Agreement (NAFTA), the predecessor to the current United States–Mexico–Canada Agreement (USMCA). Cost efficient inputs and manufacturing in Mexico support capital-intensive and higher value-added activity on the U.S. side.

For example, Taiwan’s Wiwynn (a subsidiary of electronics manufacturer Wistron) expanded production in Juarez, Mexico, of servers for U.S. data centers in 2024 and 2025. The company announced in June 2025 a $150 million investment in a manufacturing and testing facility across the border in El Paso County.

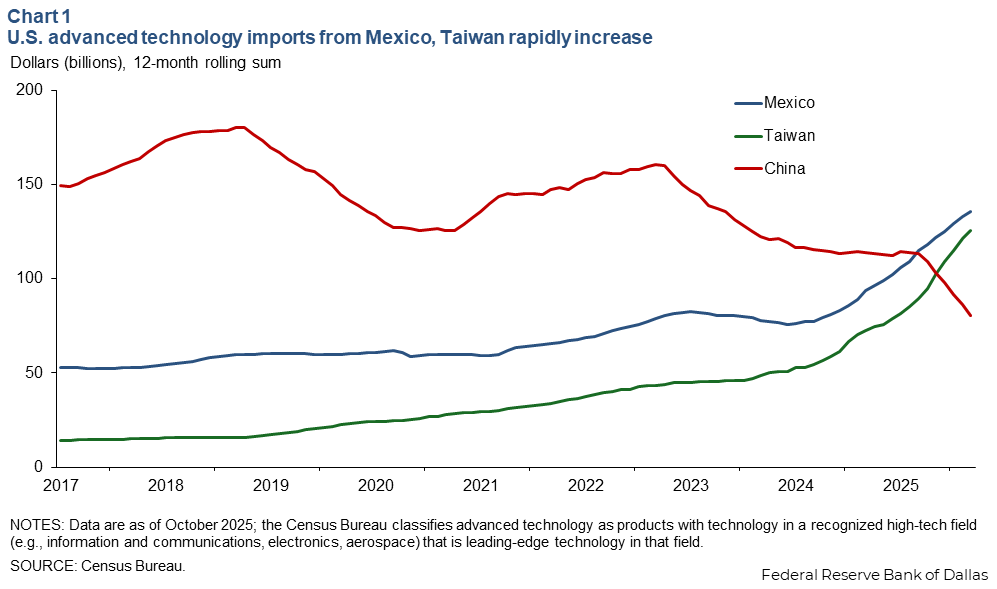

In 2025, Mexico and Taiwan both eclipsed China to become the largest sources of U.S. imports of advanced technology products, according to Census Bureau data, underscoring the importance of both economies (Chart 1).

Taiwan’s role in investment, global supply chains shifts

Taiwan companies have long played a key role in global manufacturing supply chains, particularly in the build-up of manufacturing in mainland China. More recently, Taiwan firms led efforts to diversify out of China. With a relatively small domestic market, Taiwan companies adopted a contract-manufacturing model of producing products for international brands and retailers, a significant portion of them U.S. multinational corporations.

Taiwan companies evolved in the 1990s to become original design manufacturers (ODMs), as they took on product design and research and development roles for some clients, accounting for 80 to 90 percent of global server and notebook production, for example. The largest ODM, Foxconn, manufactures and assembles iPhones for Apple, laptops for Dell and, increasingly, AI servers for the top U.S. cloud services providers.

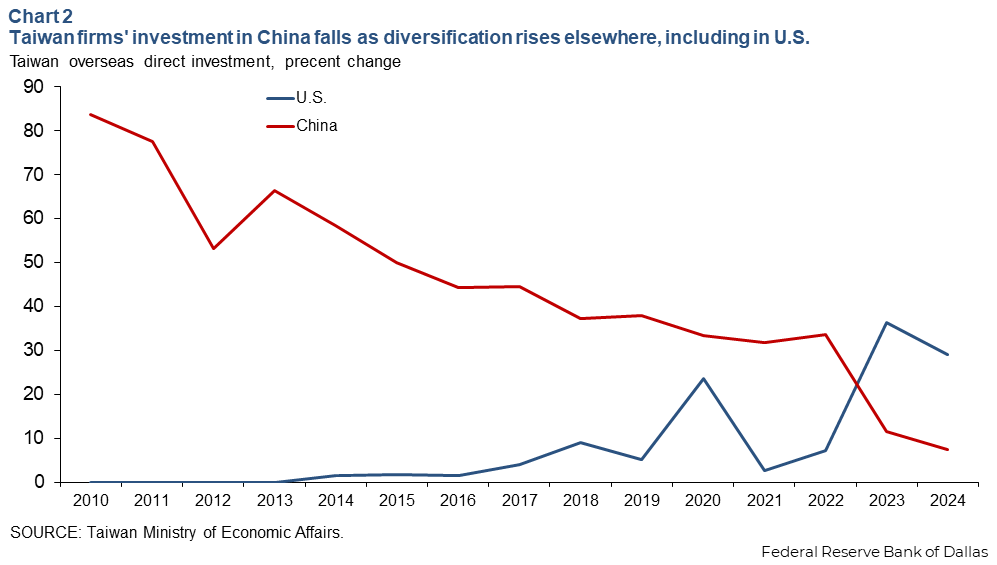

As some of the earliest foreign investors in China in the 1990s, Taiwan firms accelerated FDI following China’s 2001 accession to the World Trade Organization. Such investment in China peaked in 2010 at more than $14.5 billion, roughly 85 percent of Taiwan’s FDI, according to data from Taiwan’s Ministry of External Affairs.

Taiwan subsequently has been at the forefront of diversifying out of China, beginning more than a decade ago. While retaining significant production in China, the amount and share of Taiwan firms’ investment entering China has steadily declined since 2012, partly a reflection of higher labor costs in China, a weakening economic outlook and geopolitical risk. By 2020, China accounted for roughly one-third of Taiwan overseas direct investment, with the share falling below 10 percent in 2024–25.

Taiwan firms have shifted investments to Southeast Asia, India and Mexico, as well as back to Taiwan itself. Vietnam has been a leading beneficiary, with an accumulated stock of Taiwan FDI exceeding $40 billion, according to Vietnamese government data. Taiwan firms began reshoring, moving production back to Taiwan, in earnest in 2018–19, supported by government incentives and U.S.-China trade tensions. The impacts of Taiwan’s own reshoring are seen in Taiwan’s booming exports of advanced technology products, particularly to the U.S.

The U.S. has also become an increasingly important investment destination for Taiwan, accounting for roughly one-third of approved outbound FDI in 2023 and 2024 (Chart 2).

Taiwan investment in Mexico gains prominence

Taiwan firms have played key early roles in previous waves of Mexico’s manufacturing evolution and are similarly at the center of a pivot to high-value, advanced manufacturing in northern Mexico today. This trend is notably visible in Mexico’s export data.

In the late 1990s and early 2000s, Taiwan companies supported post-NAFTA growth in electronics manufacturing and exports, particularly involving computers. Leading manufacturer Acer was the first Taiwan company to establish manufacturing operations in Juarez, in 1998. Other Taiwan firms Foxconn, Asus, Tatung and Wistron followed, producing personal computers for brands such as Hewlett-Packard and Gateway.

Similarly, following 2018–19 U.S.-China trade tensions and USMCA taking effect in 2020, Taiwan firms were early participants in the nearshoring trend, mostly in electronics but also in automative parts and aerospace. Official Mexican data show a spike in Taiwan FDI in 2021–22, reaching $450 million. This still relatively modest amount did not put Taiwan among Mexico’s top 10 foreign investors, though Taiwan accounted for roughly 25 percent of FDI into Mexico’s computer and electronics manufacturing.

An ongoing wave of Taiwan investment in Mexico has focused on high-value, advanced manufacturing, particularly of AI hardware and servers from Taiwan’s leading ODMs.

Foxconn has the largest operations in Mexico of the Taiwan ODMs. With substantial manufacturing in Chihuahua already, Foxconn disclosed a $241 million investment in 2024 to expand its facilities in the state to produce AI servers. Foxconn also announced in October 2024 it would build in Guadalajara, Jalisco, the largest manufacturing and assembly site globally for Nvidia’s GB200 superchip, set to come online in early 2026.

Other key Taiwan ODMs, Inventec and Pegatron and Wiwynn, have opened and expanded facilities in Juarez in the past three years to produce servers, announcing investments of $75 million to $250 million. Quanta Computer disclosed large investments and a capacity expansion in Monterrey to produce AI servers and advanced electric vehicle components.

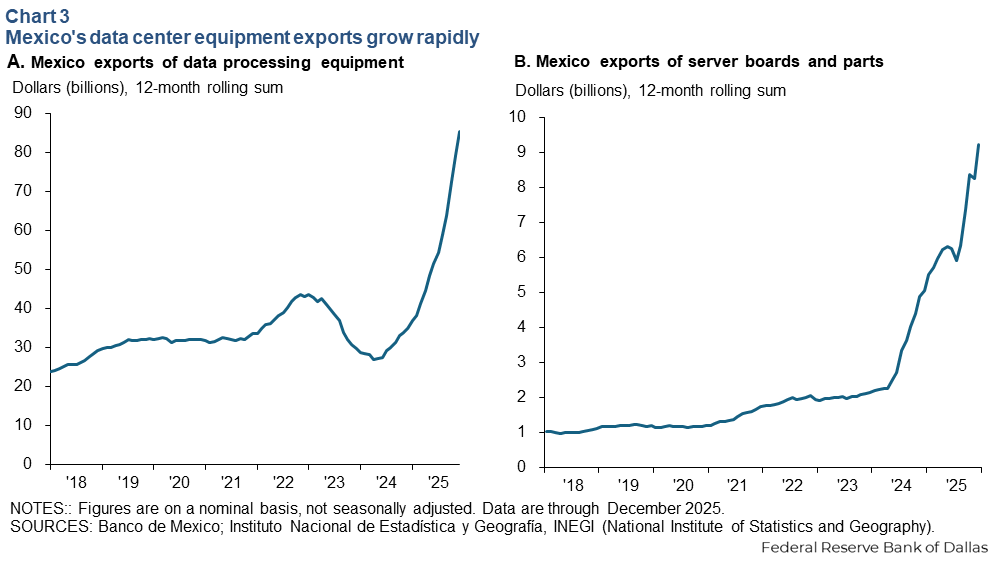

Mexico’s exports of automatic data processing machines (customs classification HS code 8471) have grown rapidly, more than doubling during the past year, to exceed $85 billion in 2025 (Chart 3).

While this includes laptop computers, the vast majority of the category consists of data servers, motherboards and components for data centers. These components are at the heart of the U.S. AI data center build-out. Chihuahua accounted for almost two-thirds of these exports in 2024.

Exports of server boards and other data server parts (HS code 8473) are growing even faster, from roughly $2 billion in 2023 to $9.2 billion in 2025.

Taiwan firms play an active, if less dominant, role in the manufacturing of other electronics products in Mexico. Fiber optic cable and wire exports, also important for network infrastructure, have grown steadily, reaching $19.6 billion in 2025. Mexico’s exports of network routers, switches and modems (HS code 8517.62) have also increased, reaching $15.6 billion over the past year after a decline in 2018–21.

LCD televisions and monitors is another important Taiwan ODM product line. Production, much of it in Baja California, significantly contributed to Mexico’s $11.6 billion in exports of these products in 2025. Lastly, Taiwan manufacturers have invested in making medical devices and electric vehicle components in Mexico.

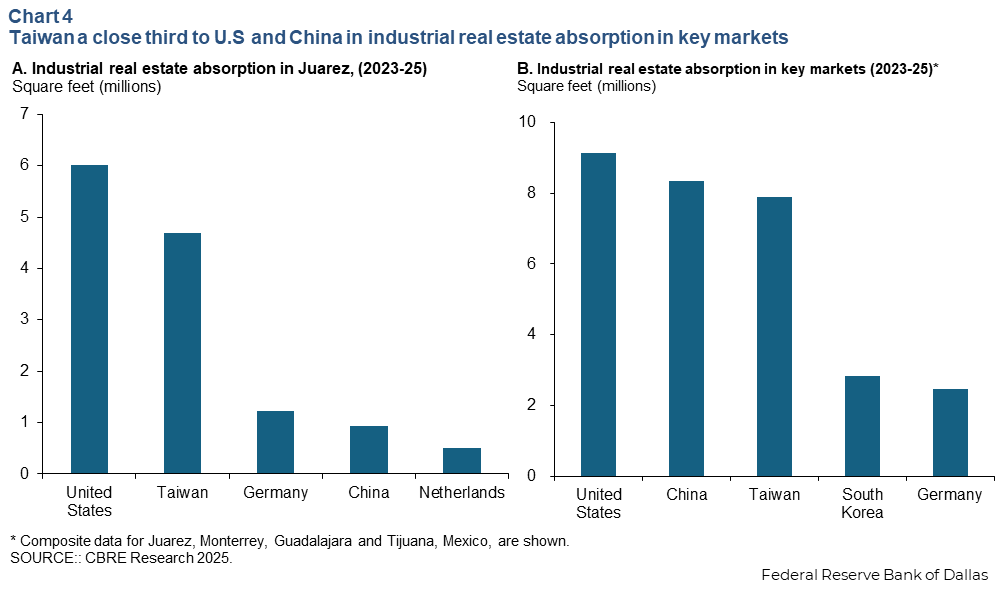

Taiwan ranked second among countries of origin in terms of absorption of industrial real estate space in Juarez by firm country in 2023–25, according to CBRE, a commercial real estate services firm. Taiwan manufacturers have absorbed 4.7 million square feet of industrial real estate space, behind only the 6.0 million square feet U.S. firms used in 2023–25 (Chart 4A).

More broadly, across Monterrey, Guadalajara and Tijuana, Taiwan ranked third, after the U.S. and China, in absorption of new industrial real estate during 2023–25 (Chart 4B). Taiwan firms ranked first in in absorption of new capacity in Guadalajara, Jalisco, the state often described as Mexico’s Silicon Valley, while ranking third in Tijuana and fourth in Monterrey. Chinese firms’ industrial real estate absorption was heavily concentrated in Monterrey, with its large automotive sector.

Taiwan investment substantially larger on the U.S. side of the border

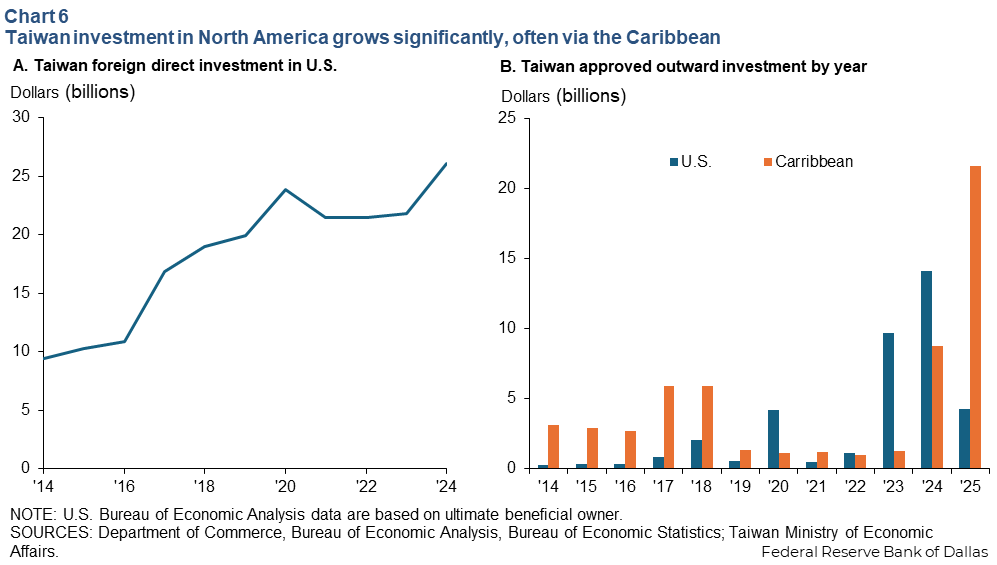

Taiwan’s FDI in the United States has grown steadily over the past decade, entering a new phase in 2025. Most notable is a large investment in semiconductor fabrication facilities in Arizona by Taiwan Semiconductor Manufacturing Co. (TSCM). The leading semiconductor firm originally disclosed a $12 billion investment in 2020, raising its planned outlay to $65 billion by 2024 and announcing plans in March for a further $100 billion over an extended number of years.

Beyond TSMC and some of its immediate suppliers, Taiwan firms have increasingly focused their U.S. investment in Texas. Global Wafers, Taiwan’s largest silicon wafer manufacturer (producing wafers that TSMC and others use to fabricate semiconductors) announced in 2022 a $3.5 billion investment north of Dallas, in Sherman, Texas. The facility came online in May 2025. Global Wafers announced a $4 billion expansion of the project in 2025 that would bring its total investment to $7.5 billion. In all, Taiwan firms have invested $13.9 billion, the State of Texas Taiwan Office reports.

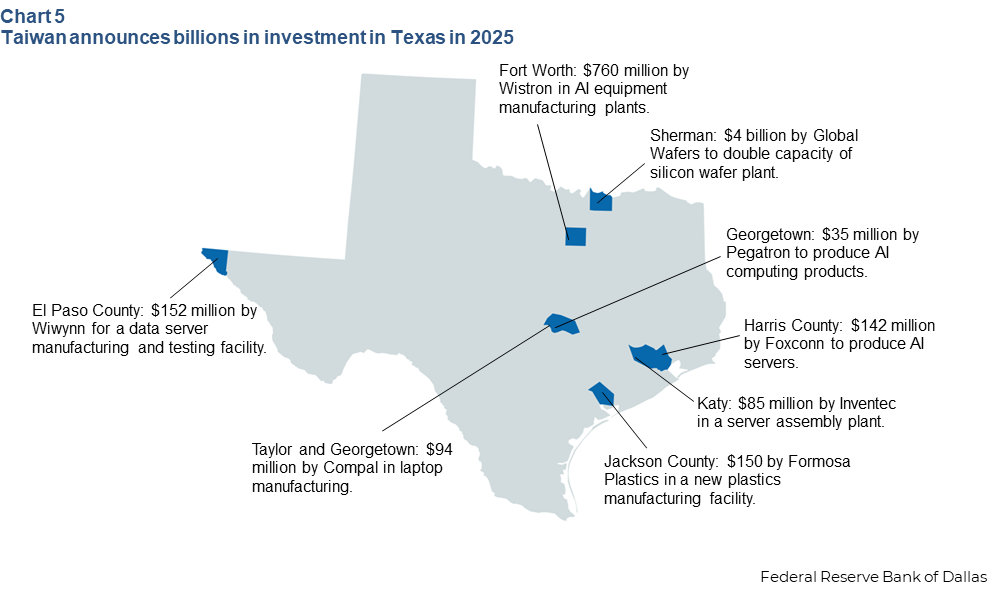

A broader range of Taiwan manufacturers—particularly the leading ODMs—announced investments in Texas in 2025. Foxconn, Inventec, Wistron and Pegatron unveiled plans to build AI servers in Texas. For Inventec, Wistron and Pegatron, the plans marked their first manufacturing operations in the U.S. Each company has sizeable manufacturing capacity in Northern Mexico that can support the U.S. operations with critical supply chain inputs (Chart 5).

Announced investments do not always materialize at the planned scale cited or within specified timeframes. However, increased activity is evident in both official U.S. and Taiwan data. Bureau of Economic Analysis Statistics data show a steady pickup in the stock of Taiwan FDI in the U.S. during recent years, reaching $26 billion in 2024 (Chart 6).

Taiwan data on external investment (which requires government notification and approval) are likely more comprehensive and forward-looking. Taiwan data show an uptick in approved annual investment to the U.S. of $9.7 billion in 2023 and $14.1 billion in 2024.

A significant portion of Taiwan investment goes through holding companies in Caribbean offshore financial centers—$8.8 billion in 2024 and $21.6 billion in 2025—according to data from Taiwan’s Ministry of Economic Affairs. Although it is not possible to break down these funds’ ultimate destination, most likely a significant portion will end up in the U.S. and Mexico.

While there is a degree of uncertainty about themagnitude of U.S. data center growth and demand for related equipment, the waveof construction appears closer to the beginning than the end of its build-out. The Electric Reliability Council of Texas in its latest electricity load forecast projects new data centers in Texas to add more than 24 gigawatts of power demand by2031. Such growth could support significantly more equipment production inMexico and Texas in the years ahead.

About the author

Brendan Kelly is a former visiting fellow at the Federal Reserve Bank of Dallas Global Institute.