Mexico gains from U.S.-China trade war; inefficiencies limit benefit

A sequence of major economic and geopolitical events has reshaped the structure of global trade in the past decade. It began with U.S. imposition of tariffs on Chinese goods in 2018. The postpandemic followed with widespread disruption to global value chains—the process of manufacturing a product in stages across several countries. Along the way, trade fragmentation associated with geopolitical tensions increased, most notably after Russia invaded Ukraine in 2022.

The events collectively triggered a significant reconfiguration of international sourcing patterns. Recent studies have described this phenomenon as a Great Reallocation in U.S. sourcing, away from a narrow set of countries, particularly China. A central question for policymakers is whether the observed reallocation has meaningful macroeconomic consequences beyond changes in bilateral trade shares. In particular, has the diversion of U.S. sourcing away from China translated into measurable gains in Mexican aggregate output, such as higher GDP growth?

We estimate that trade diversion from China should have increased Mexico’s GDP by up to 1 percent by incentivizing additional investment. The results underscore how domestic investment dynamics shape macroeconomic gains from shifting global trade patterns.

Mexico benefits from sourcing pattern changes

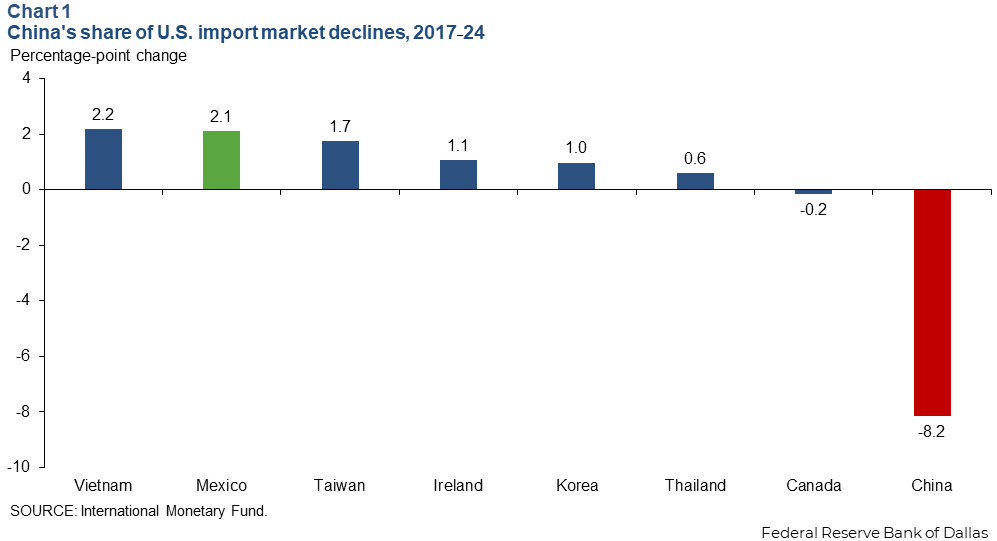

China’s share of U.S. imports declined between 2017 and 2024, while the shares of several alternative suppliers correspondingly increased (Chart 1). Among these, Mexico stands out, becoming the U.S. top manufacturing partner in 2022 and No. 1 overall trading partner the following year.

Mexico occupies a distinctive position among countries meeting part of U.S. demand previously satisfied by Chinese exports. Mexico’s geographic proximity, long-standing participation in North American production networks and political alignment with the U.S. make it a natural candidate for nearshoring and an attractive destination for friendshoring.

Measuring the impact from this reallocation requires its effects to be isolated from other factors shaping GDP growth in Mexico. Over the past decade, the country has faced significant and persistent economic crosscurrents, including rising labor costs, an appreciating peso, U.S. manufacturing sector weakness, fiscal constraints and uncertainty about U.S. tariff policy and renewal of the United States-Mexico-Canada Agreement. All have hindered and continue to diminish economic growth in Mexico.

U.S.-China trade war provides policy insights

The U.S.–China dispute offers a compelling natural laboratory to study trade diversion. Although multiple geo-economic developments have contributed to the broader Great Reallocation, the escalation of tariffs between the United States and China stands out as the principal catalyst. Importantly, this increase in bilateral trade costs between the United States and China caught many by surprise. It represents an exogenous shift in trade policy that allows examination of how third-party countries, such as Mexico, adjust.

The Trump administration initiated the trade dispute when it imposed new tariffs on Chinese imports in 2018, prompting retaliatory tariffs on imports from the U.S. In the nearly eight years since then, China has gradually lost ground as a top U.S. trading partner.

A substantial body of research has documented the economic consequences for the United States and China. However, comparatively less attention has been devoted to its effects on other economies, beyond the well-documented reconfiguration of global trade flows from China, toward alternative suppliers including Mexico. Understanding the implications for third-party countries requires moving beyond relative trade flows and examining changes in absolute demand and domestic production.

While changes in trade shares presented in Chart 1 provide indications of shifting demand patterns, they do not, by themselves, reveal the net impact on demand and, therefore, production.

More specifically, an increase in Mexico’s share of U.S. imports still does not necessarily imply an aggregate increase in U.S. demand for goods produced in Mexico. If higher tariffs on Chinese imports reduce overall U.S. demand for imported goods, Mexico’s larger share could coincide with stagnant or even declining absolute exports.

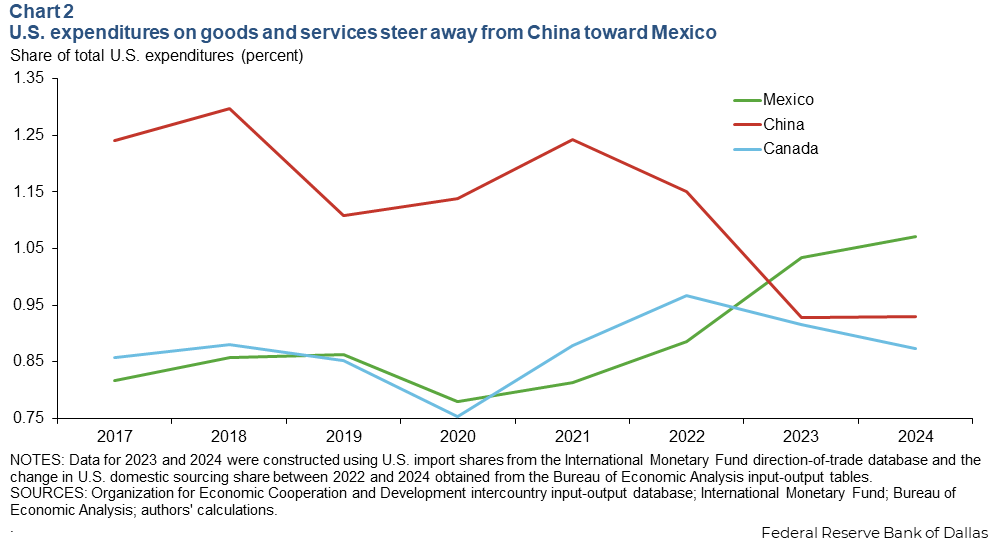

Changes in total U.S. expenditure on Mexican goods—rather than solely shifts in import shares—provide a clearer view of net demand effect (Chart 2). There was a clear increase in U.S. demand for goods produced in Mexico during 2017–24, suggesting that output in Mexico expanded to meet this increased demand in response to the China trade tensions.

Ongoing research shows that Mexican exporters in a number of industries increased not only exports to the United States, but also output and employment in response to the trade war. These findings suggest that the reallocation of U.S. imports toward Mexico may have generated tangible real effects within the Mexican economy, rather than merely reshuffling trade shares across countries.

Trade diversion affects not only exporting firms but also domestic suppliers, labor markets, intermediate input linkages and relative prices. Quantifying the aggregate impact of the U.S.–China trade war on Mexico requires a theoretical representation or model of the world economy that captures these interdependencies. Such a framework must account for changes in trade policies across countries and trace their effects through production networks, rather than holding other elements of the global economic landscape fixed.

Assessing U.S.-China trade war impact on Mexico’s GDP

To quantify the macroeconomic consequences of the U.S.–China trade war for Mexico, we rely on a multi-country, multi-sector general equilibrium trade model of the type widely used to evaluate the aggregate effects of trade policy changes. While similar models have been used to study the U.S. and China, we focus on Mexico as a third-party economy exposed to trade diversion. This approach allows us to move beyond reduced-form correlations and instead trace the full set of adjustments triggered by increased U.S.–China trade barriers.

The model captures several key features of the global economy essential for assessing aggregate effects. First, it includes multiple countries connected through trade in intermediate inputs, enabling the analysis of global value chains and cross-border production linkages. Second, it incorporates sectoral input–output linkages, so that changes in trade costs in one industry propagate through upstream and downstream sectors. Third, production relies on multiple factors, capital, skilled labor and unskilled labor. The model allows heterogeneous distributional effects and factor reallocation across sectors. Finally, the framework allows long-run adjustments in investment and capital accumulation. They are crucial for evaluating persistent changes in GDP rather than transitory fluctuations.

Within this structure, we examine the effects of the tariffs implemented during the U.S.–China trade war on Mexico’s GDP. The central mechanism operates through trade diversion. Higher U.S. tariffs on Chinese goods reduce the competitiveness of Chinese exports in the U.S. market, thereby shifting U.S. demand toward alternative suppliers, including Mexico. The model enables us to quantify how much of this redirected demand translates into higher Mexican production, income and ultimately GDP after taking into account associated changes in wages, prices and trade balances.

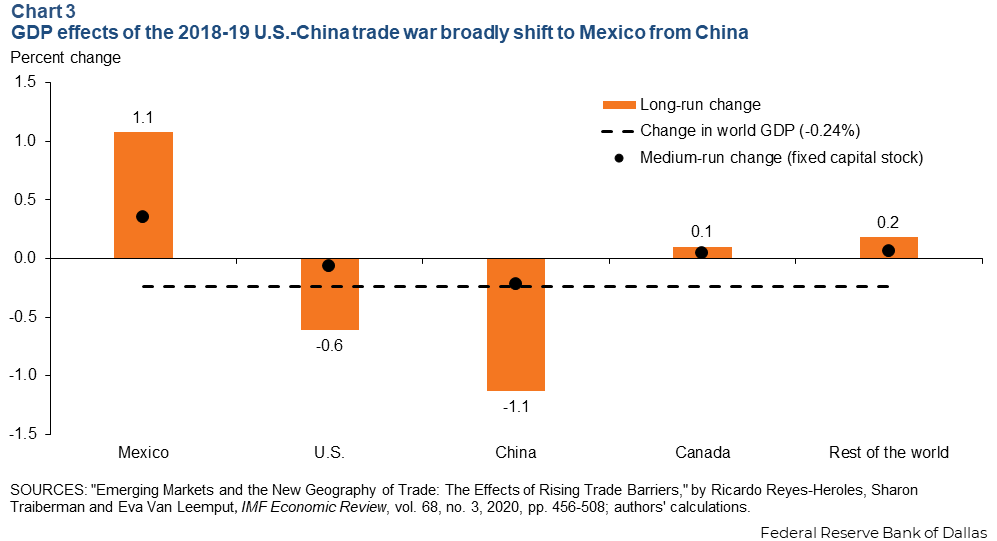

The simulation indicates the U.S.–China tariff shock generated a positive effect on Mexico’s GDP, shifting U.S. demand from goods produced in China toward those produced in Mexico (Chart 3).

In the medium run—a period when aggregate capital does not change through investment—Mexico experiences a modest increase in GDP of 0.35 percent, driven primarily by higher exports to the United States and expansion of sectors integrated into North American value chains.

In the long run, once Mexico’s capital stock used for production adjusts, GDP expands by an additional 0.73 percentage points (total of 1.08 percent), reflecting increased investment in expanding industries. Capital accumulation amplifies the medium-run effect by a factor of slightly more than three, underscoring the importance of investment dynamics when evaluating the macroeconomic consequences of trade policy shocks.

What about the effects on the countries participating in this trade war? In line with existing studies, we find that output in the U.S. and China was negatively affected by the trade war. Higher tariffs increase the prices of imported goods, which leads to lower real income for households and a drop in production efficiency by firms.

Our results suggest small negative GDP effects for the U.S. of -0.09 percent and for China of -0.23 percent in the medium run. These magnitudes are in line with those obtained by studies considering similar models to study effects of the U.S.–China dispute.

However, in contrast to those studies, our model allows us to account for the effects in the long run, a horizon when investment adjusts to new trade incentives, thereby altering the economies’ productive capacity. Over this horizon, the effects are amplified considerably by a factor of approximately six, reflecting the sizable contraction in investment and therefore available capital for production.

Additionally, even though Canada and Mexico share proximity and political alignment with the United States, positive spillover effects for Canada are minuscule relative to Mexico. The large spillovers for Mexico arise because Mexico is better suited than Canada to take the place of China in production of tariffed goods. Mexico’s comparative advantage profile is more similar to that of China that that of Canada.

What has limited Mexico’s expansion?

Our results indicate that trade diversion from China to Mexico translated into a sustained increase in Mexican output rather than a temporary export surge. Importantly, however, the magnitude of the GDP expansion depends critically on the economy’s ability to adjust through investment.

When capital accumulation responds over time, sectors benefiting from increased U.S. demand are able to expand their productive capacity, amplifying the overall impact. In our estimates, endogenous investment raises GDP by roughly 1.1 percentage points permanently compared with only 0.4 percentage points when the capital stock is held fixed.

Importantly, the model provides an estimate of the increase in GDP generated exclusively by trade spillovers, but it misses other important forces that may have affected the Mexican economy’s subsequent performance and counteracted these positive effects.

For instance, Mexico’s transition from the North America Trade Agreement to the successor United States–Mexico-Canada agreement strengthened auto sector content rules when it took effect in 2020. Such regulatory changes may have trimmed GDP gains from the U.S.–China trade dispute. Other long-run structural changes, such as Mexico’s reversal of earlier energy sector reforms, weaker productivity growth, and increased levels of crime and violence became increasingly important constraints on output growth.

Thus, although trade reallocation has contributed to economic growth in Mexico, structural constraints led to underperformance. Absent the positive spillovers generated by trade diversion associated with third-country disputes, Mexico’s economic performance would likely have been weaker.

About the authors

Ricardo Reyes-Heroles is a principal research economist in the Research Department at the Federal Reserve Bank of Dallas.

Luis Torres is a senior business economist in the San Antonio Branch of the Federal Reserve Bank of Dallas.

Diego Morales-Burnett is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.