Texas economic activity strengthens despite slowing job growth, greater price resistance

Texas employment growth slowed even as overall activity strengthened in August and September. Resistance to price increases rose.

Employment expanded 1.1 percent in August, down sharply from 3.8 percent in the first half of 2023. Meanwhile, respondents to the Texas Business Outlook Surveys (TBOS) reported faster service sector growth along with rebounding manufacturing production. They also noted, however, that price pressures were stable in recent months.

TBOS respondents in August lowered their selling price and wage growth expectations for the year relative to what year-end expectations were in May. There was no downward revision of input cost growth, however, likely reflecting higher energy prices. The price of benchmark West Texas Intermediate crude oil has risen more than 20 percent to near $90 per barrel in the past year.

Employment growth slows in August

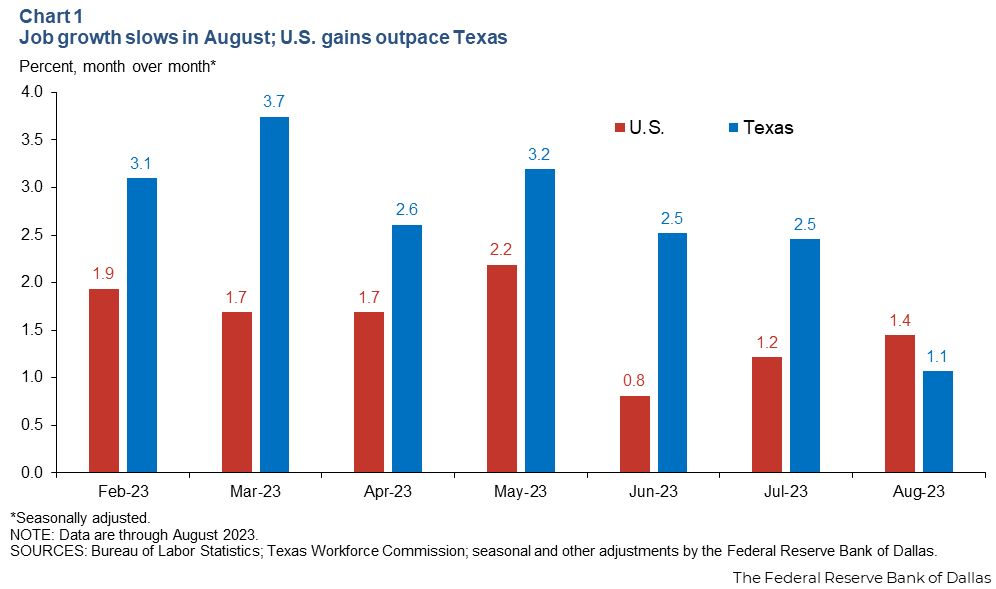

Texas job growth slowed in August, expanding only 1.1 percent at an annualized rate, equivalent to adding 12,401 jobs (Chart 1). By comparison, the nation’s employment grew 1.4 percent, outpacing Texas for the first time since November 2022.

Texas job growth had remained robust over the past year amid higher interest rates, falling manufacturing production and fears of recession. It is unclear whether the recent result indicates actual slowing or is a statistical anomaly.

Given strong job growth earlier this year, the Dallas Fed’s Texas Employment Forecast is now 2.9 percent for 2023 (December over December), implying growth of 2.1 percent, annualized, through the end of the year. Though lower than previous forecasts, this would still be stronger growth than Texas’ long-term, 2 percent trend annual employment growth rate.

Declining job openings and rapid labor force expansion have helped rebalance the state labor market since late 2021. The share of firms hiring has fallen from near 70 percent at its peak to nearly 50 percent in July. About half of those firms looking for workers reported that a lack of applicants is impeding their ability to hire, compared with three-quarters saying they were similarly constrained in July 2021.

Despite less-tight labor markets, some TBOS firms continue to report trouble finding qualified workers in particular areas. One administrative services contact said, “Skilled labor is still hard to find for our business. We have increased our hiring pay by 22 percent and cannot find qualified candidates.”

Manufacturing rebounds as service sector stays strong

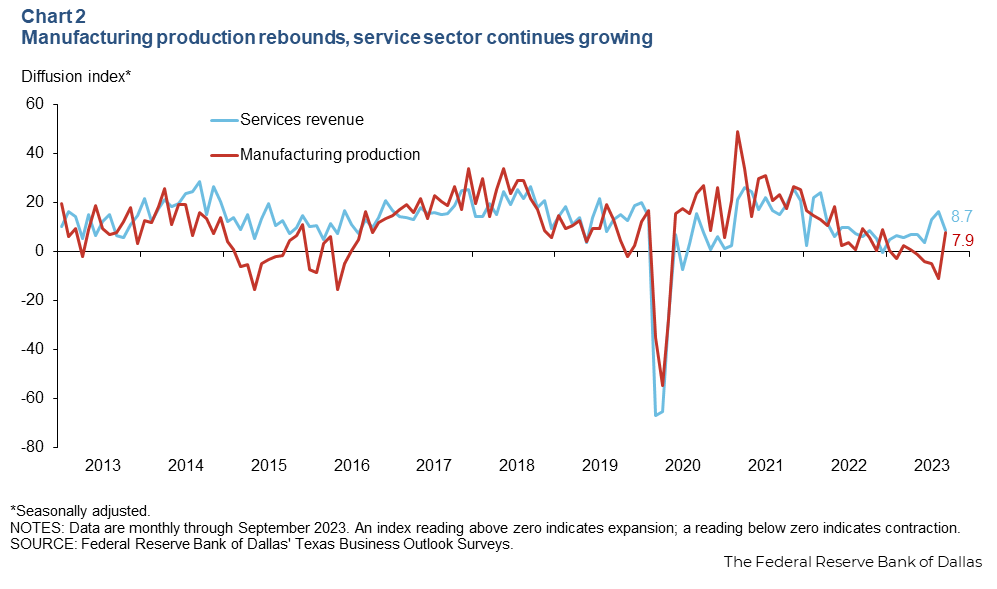

There were positive output signs, especially in the goods sector, in the September TBOS. Manufacturing production expanded after contracting for four months (Chart 2). However, services revenue growth declined following a surge in August.

Overall, company outlooks remained pessimistic, which may mean a short-lived upturn. Comments were overwhelmingly negative, citing downside risks including the United Auto Workers national strike, the possibility of a federal government shutdown, weak demand in China, falling housing activity, troubled commercial real estate markets and difficulty passing on higher costs to customers.

Price pressures stable despite sharply higher input costs

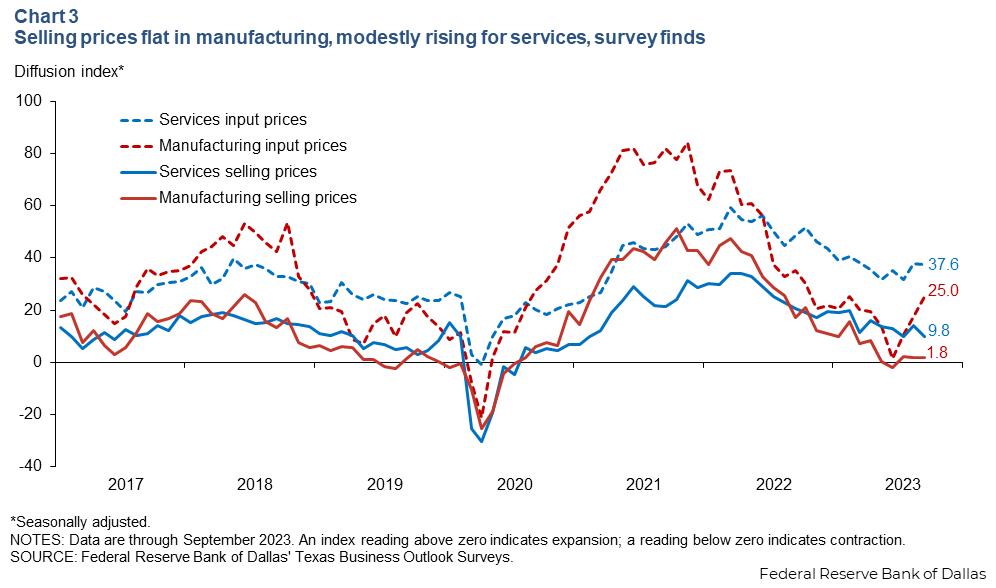

Selling prices in September increased at about the same pace as in August in both the service and manufacturing sectors (Chart 3). Manufacturing input price pressures surged, however, possibly the result of higher energy prices.

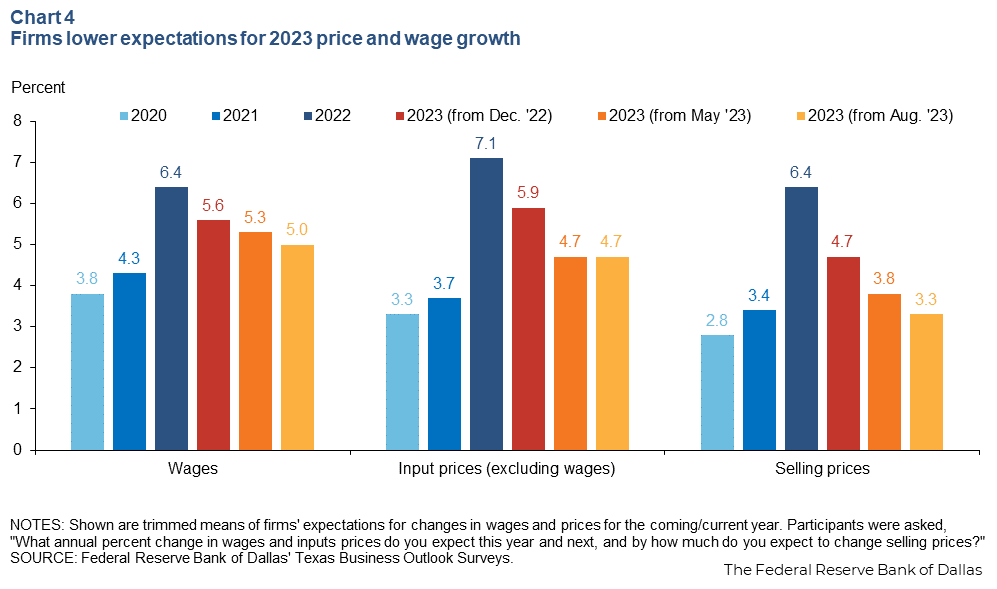

Despite heightened cost pressures, Texas firms lowered their expectations for price and wage inflation, according to TBOS special questions in August (Chart 4). Selling prices were expected to rise 3.3 percent between December 2022 and December 2023, down from a 3.8 percent expectation in May.

Cost growth expectations did not change over the summer, as firms still anticipate 4.7 percent growth, while wage growth expectations fell only slightly (from 5.3 to 5.0 percent). Thus, the decrease in selling prices does not appear to be a product of cheaper inputs, but likely of limited ability to pass costs on to customers.

In their comments, TBOS respondents confirmed this situation. “[The] cost of goods sold continues to increase beyond [firms’] ability to raise prices,” one TBOS respondent said. Another noted a change in consumer attitudes, saying, “Customers were willing to accept practically any price increase over the last couple of years, [but] we are starting to see resistance to continued price increases.” That firm also reported it “expect[ed] more resistance going forward,” potentially making it even more difficult to pass through costs.

About the authors

Diego Morales-Burnett is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.

Pia Orrenius is a senior economist at the Federal Reserve Bank of Dallas.

Ana Pranger is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.