Inflation forecasts based on money growth proved accurate in 2021, though generally unreliable

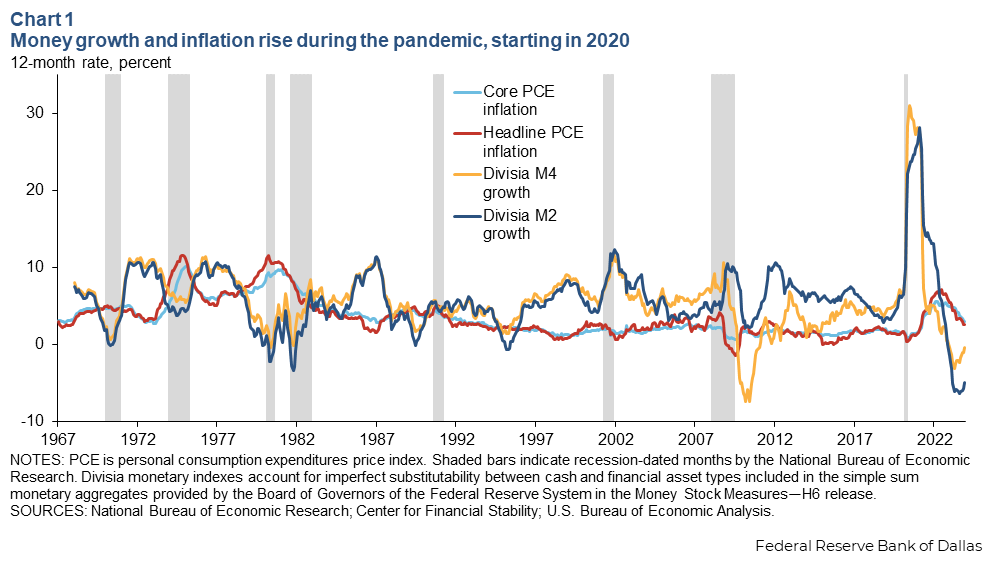

Most forecasters and policymakers were surprised by the degree and persistence of high inflation in 2021 and 2022. These large misses in predicting inflation were preceded by an unprecedented level of money growth, bringing renewed attention to quantity-theoretic linkages between inflation and money growth (Chart 1).

Some analysts view high inflation in 2021 and 2022 as unsurprising and a predictable consequence of rapid money growth. Indeed, a simple forecast using only lagged inflation and money growth would have signaled the rise of inflation starting in early 2021 and the disinflation throughout 2023 relative to the 12 previous months.

Yet, to rely on a forecast in real time, it must be robust across time periods. We show that this simple forecast would have underperformed in the two decades before the pandemic, because the unstable relationship between inflation and money growth makes forecasting impractical.

Quantity equation versus quantity theory

Understanding the quantity equation is key to thinking about the connection between money growth and inflation. The quantity equation is an accounting identity that must hold true for every period. It states that the nominal value of all transactions in an economy within a period equals the product of the quantity and velocity of money.

Nominal GDP, the product of the price level and real output, is typically used to measure the dollar value of all transactions within an economy. The velocity of money refers to the average number of transactions for which a single money unit is used within a period. It is measured by dividing nominal GDP by a measure of the stock of money.

An implication of the quantity equation is that price level growth, inflation, equals money growth minus the difference between real output growth and money velocity growth. That is, money growth is linked to inflation via this accounting identity, independent of how you think the economy works—for example, directions of causality among these variables.

The quantity theory of money assumes that real output growth, net of velocity growth, is largely determined independent of monetary policy. This assumption implies that changes in money growth, other things equal, translate one-for-one into changes in inflation. Or, in other words, the money growth–inflation link is strong.

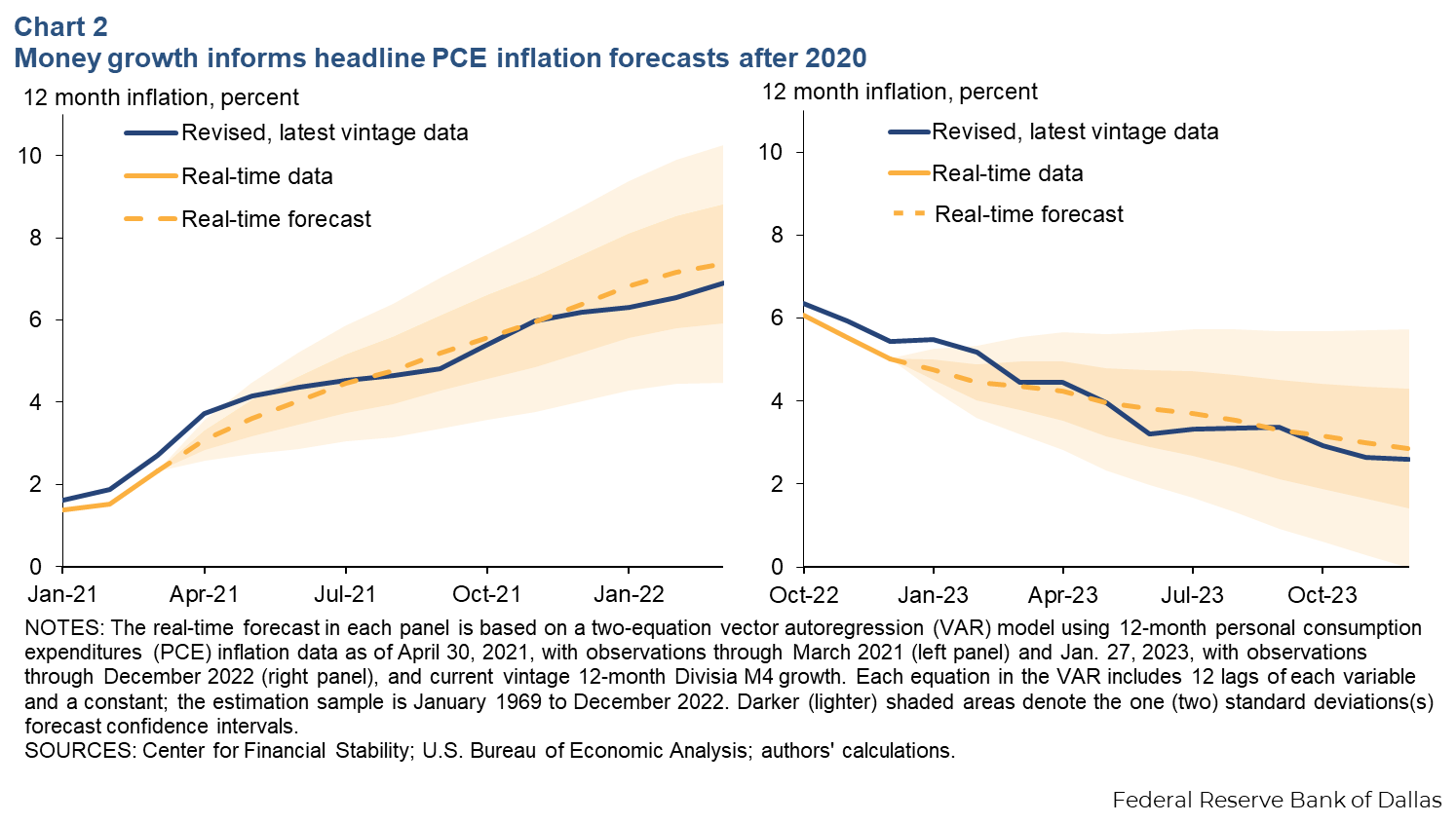

If the link between money growth and inflation is strong, then money growth should provide useful information for forecasting inflation. In fact, inflation forecasts from a simple two-equation vector autoregression model, with observable money growth and inflation, predicted the inflation pickup in 2021 and the elevated inflation in 2022.

Chart 2 shows forecasts for the path of 2021 and 2023 headline personal consumption expenditures (PCE) inflation using the same model with real-time inflation data through 2020 and 2022, respectively. We measure money growth using current vintage 12-month Divisia M4 index growth. Divisia indices are preferred to simple sum monetary aggregates, such as M2, because they weigh each component found in the simple sum measure (components such as cash in circulation and bank deposits) by the degree to which the component serves as money.

Taking stock, the quantity equation is a useful way to think about the relationship between money growth, inflation and real output growth, whereas the quantity theory imposes an assumption on these relationships. Furthermore, forecasting inflation using a model with money growth inspired by the quantity theory has performed relatively well at predicting the realized path of inflation after 2020.

Forecasting inflation with money growth in a two-equation model

If this forecast specification accurately signaled the past several years of inflation, why was the rise and persistence of inflation a surprise to most forecasters?

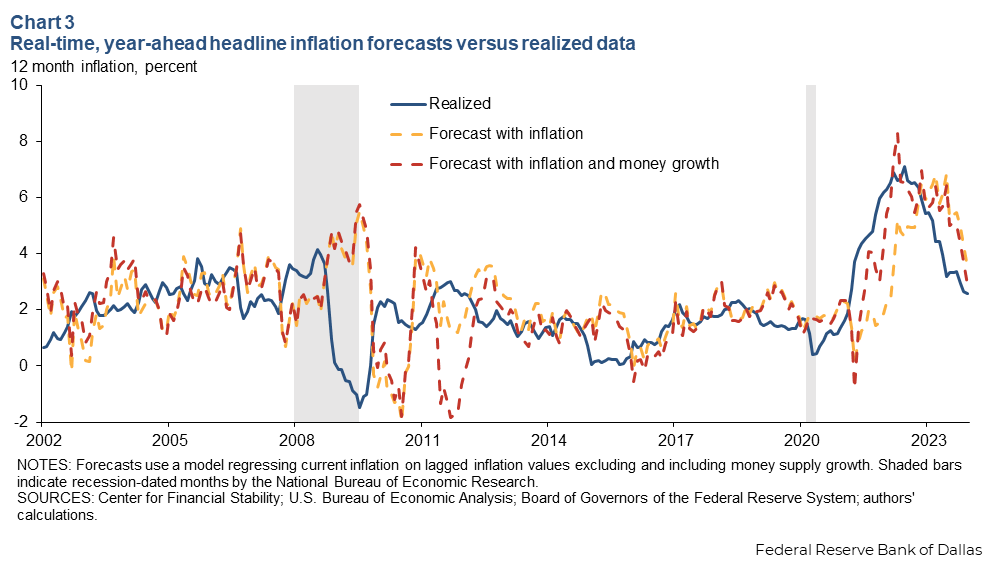

To be relied upon when forming real-time forecasts, the signal from money growth must be useful in general, not just during the period following the 2020 recession. To evaluate if this is the case, we generate real-time inflation forecasts from January 2002 to December 2023 using the two-equation vector autoregression model behind the forecasts in Chart 2. The estimation sample starts in 1969 and ends with the most recent data at the time the forecast would have been made.

Chart 3 provides a time series of year-ahead, 12-month headline PCE inflation forecasts using this model. We also show inflation forecasts at the same horizon from a model that regresses current inflation on lagged values of itself, excluding money growth.

In general, the forecast that includes money growth information does not vary much from the lagged inflation-only forecast. Discrepancies between the two forecasts (yellow and red lines) are pronounced in late 2011, when the money growth forecast predicts significant deflation, and in 2021. The money growth forecast performed better after 2020, predicting the sharp rise in inflation in 2021. However, money growth provides limited additional information for forming accurate year-ahead, 12-month inflation forecasts before 2020 or during the recent period of disinflation.

To quantify the relative performance of the inflation-only and inflation-plus-money-growth forecasts, we compute the root mean square error (RMSE)—the size of a typical forecast miss—for each, presented in Table 1. We compute the RMSE for pre-2020, post-2020 and the full sample. We also perform the same forecast with alternative Divisia monetary index growth measures and alternative inflation measures. Finally, we compare the RMSE calculations to simply forecasting inflation will be 2 percent, the Fed’s longer-run target level.

| Table 1: Relative performance of year-ahead, 12-month inflation forecasts | ||||||

| Headline | 2 percent | No money | Divisia M4 | Divisia M4- | Divisia M3 | Divisia M2 |

| Pre-2020 | 1.02 | 1.70 | 1.83 | 1.83 | 1.77 | 1.71 |

| Post-2020 | 2.81 | 2.22 | 1.46 | 1.95 | 1.96 | 1.79 |

| Full sample | 1.52 | 1.80 | 1.77 | 1.85 | 1.81 | 1.73 |

| Core | ||||||

| Pre-2020 | 0.49 | 0.68 | 0.93 | 0.93 | 0.87 | 0.75 |

| Post-2020 | 2.23 | 1.59 | 1.42 | 1.53 | 1.58 | 1.96 |

| Full sample | 1.05 | 0.92 | 1.04 | 1.07 | 1.03 | 1.01 |

| Trimmed mean | ||||||

| Pre-2020 | 0.45 | 0.55 | 0.59 | 0.61 | 0.60 | 0.57 |

| Post-2020 | 2.81 | 1.26 | 1.35 | 1.31 | 1.33 | 1.34 |

| Full sample | 1.52 | 0.73 | 0.79 | 0.79 | 0.79 | 0.77 |

| NOTE: Trimmed mean PCE inflation is available beginning in 1978, so the estimation sample for forecasts of trimmed mean inflation begins in 1979 due to included lags in the model specification; “2 percent” assumes that the inflation forecast equals the Federal Reserve’s 2 percent inflation target; “No money” is a forecast from a single equation model with no money growth measure; Divisia M2, M3, M4- and M4 are various monetary indexes, each of which includes additional financial assets intended to capture a broader definition of money while adjusting for the substitutability between currency and each financial asset type. SOURCES: Center for Financial Stability; U.S. Bureau of Economic Analysis; Federal Reserve Bank of Dallas; Board of Governors of the Federal Reserve System; authors’ calculations. |

||||||

Since 2020, forecasts that include money growth generally, although not uniformly, outperform the benchmarks of guessing 2 percent or excluding money growth. However, before 2020, inflation forecasts using either of these benchmarks, 2 percent or excluding money growth, would have been more accurate.

Over the full sample, from 2002 to 2023, money-based forecast performance is similar to or worse than the benchmarks.

The case is not at all clear that money growth measures are useful for forecasting inflation. That being said, these results should not be overextended. We have tested one specification for forecasting inflation with money growth. Other specifications may be more accurate over long samples.

These results also do not imply that money growth does not matter for inflation; as we noted, the quantity equation must hold. However, as money demand changes, and in particular as money velocity fluctuates with interest rates, this relationship can become unstable with money growth providing limited useful information for inflation forecasting.

About the authors

Tyler Atkinson is a senior business economist in the Research Department at the Federal Reserve Bank of Dallas.

Ron Mau is a senior business economist in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.