Oil prices are up; whither the Texas boom?

As the nation’s largest energy-producing state, Texas benefits from higher oil prices on net. Refined products, natural gas and petrochemicals flow from Texas to the rest of the country and the world. Higher oil prices have historically led to increased oil and gas activity that ripples through the state economy, boosting employment and state GDP.

However, the current economic landscape differs significantly from previous oil shocks and may only modestly increase domestic oil production, providing a comparatively mild state economic impact. Uncertainty about how long oil prices will remain elevated is tempering opportunism in an industry that appears far more financially disciplined than in the past.

Finally, the state’s economy is more diversified than during previous oil price run-ups, and oil and gas production is much more efficient, requiring fewer workers to produce the same or greater output. Nonetheless, energy sector gains come as car-dependent Texans confront higher pump prices and diminished purchasing power.

The genesis of sharply higher oil prices is the Iran conflict and constriction of shipping traffic through the Strait of Hormuz, the narrow waterway connecting the Persian Gulf with the Gulf of Oman. It is the conduit through which roughly 20 percent of the world’s crude oil, refined products and liquified natural gas flows.

The average West Texas Intermediate (WTI) crude spot price spiked from $63 per barrel for the week ended Feb. 6, 2026, before the conflict, to $106 during the week ended April 3. Over the 12 weeks ended May 29, the front-month closing price of WTI futures averaged almost $100.

Texas oil and gas production lead U.S.

Since the discovery of oil at Spindletop in 1901 , the oil and gas industry has been an economic driver in Texas. Texas produced 5.8 million barrels of oil per day (mb/d) in 2025, accounting for 43 percent of total U.S. production. Were Texas a nation, its crude oil output would rank fourth globally, behind Russia, Saudi Arabia and the rest of the United States.

Upstream activities, such as exploration and production, are only one portion of the oil and gas industry. Downstream industries—refining and petrochemicals—convert oil, natural gas and natural gas liquids (ethane, propane and butane) into products such as gasoline and basic chemicals.

Texas is home to nearly 30 percent of U.S. refining capacity and more than 75 percent of U.S. basic chemical production capacity. Much of what the state produces is exported. Texas accounts for 57 percent of U.S. petroleum and coal product exports and 31 percent of chemical exports (excluding pharmaceuticals). Altogether, $117 billion in chemical and petroleum product exports originated in Texas in 2025, 5.3 percent of the nation’s total exports.

The upstream oil and gas industry made up 7 percent of state GDP on average from 2019 through 2024. Including midstream (pipeline transportation), downstream and other closely related manufacturing activities (heavy machinery and fabricated metal products) raises that share to 15 percent.

Despite this substantial contribution to output, the energy industry’s employment share is quite small. Upstream industries accounted for just 1.4 percent of jobs in Texas on average from 2020 through 2025. The inclusion of midstream, downstream and related manufacturing industries increases the share to 4.3 percent.

Many service sector firms closely tied to the energy sector are not included in these shares. Among those are logistical services, scientific, engineering and technical services, legal services, and banking and energy finance.

Previous oil price spikes were beneficial

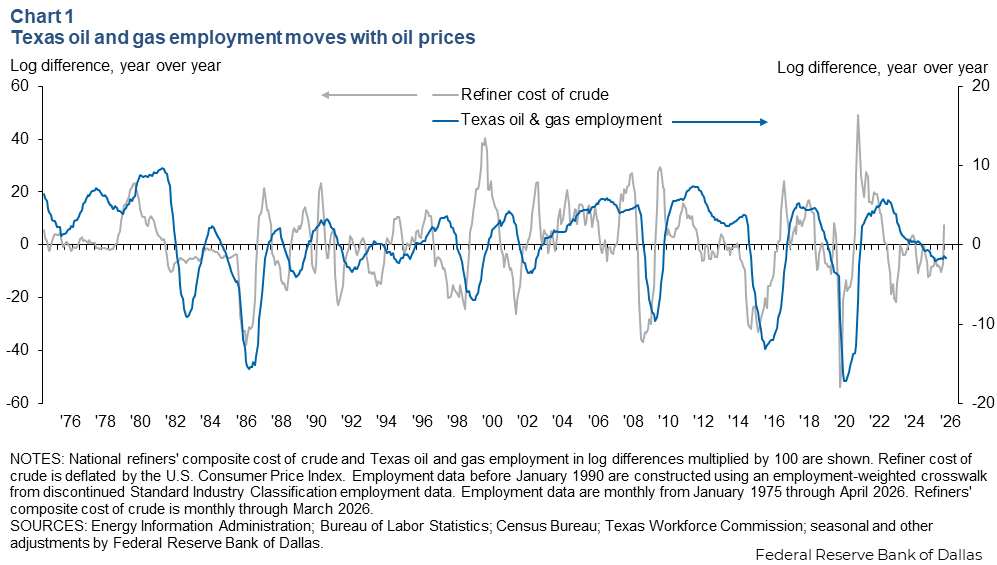

Rising oil prices historically have boosted producers’ revenues and expected profits, resulting in higher capital expenditures and hiring, albeit with a lag (Chart 1).

Previously, when the price of oil rose, it took two to three months for the number of active drilling rigs to increase. Employment gains usually closely follow rig activity. Jobs in oilfield services, fabricated metal product manufacturing and oilfield machinery manufacturing are the first-to-hire (and first-to-fire) sectors. Even there, workforce changes depend on such variables as slack in the oilfield labor force, availability of idle rigs and the scale of the change in activity.

Models predict a 0.6 to 1.6 percentage point increase in Texas job growth between March 2026 and March 2027 in response to a sustained 66 percent increase in oil prices. Applying this to last year’s employment growth rate of 0.7 percent, a similar oil price shock would have lifted Texas job growth to between 1.3 and 2.3 percent.

We construct this range of effects by drawing on previous work at the Dallas Fed, using data from 1990–2025 and by rescaling results from other academic work to the current price shock.

Compared with more recent periods, estimates using historical data and older research find oil prices previously provided a much larger impact on the state economy. The changes since the 1970s and 1980s are likely due to Texas diversifying away from oil and gas. With significant growth in business services and high-tech industries, the tight relationship between oil prices and Texas employment has likely weakened. The same developments are even observed in Houston, the nation’s energy capital.

Disentangling the various effects of oil prices on aggregate demand and supply is notoriously difficult, and the calculated impacts assume high oil prices are a sustained, one-time shift. The nature of the Iran conflict and the Strait of Hormuz shutdown leaves considerable uncertainty about the persistence of elevated oil prices. A temporary shock would have smaller effects on the state than the models suggest.

How Texas gains from higher oil prices

Increased capital expenditures and employment among energy producers make up the most important channel through which the state economy benefits from a lasting oil price spike. Other drivers include worker wages, royalty payments, tax revenues and even increased bank lending.

A material increase in shale oil production requires investment in drilling rigs and new equipment, resulting in higher real GDP across multiple industries. There are some marginal alternatives to new exploration. Upgrading older wells increases production near term, and accelerating shale well completions pulls future production forward.

When drilling increases, it boosts orders for a wide range of products, such as generators, drill bits, explosives, tubular goods and chemicals. Hiring subsequently increases both in the oil field and throughout the supply chain. Estimates for job multipliers suggest that each new oilfield position supports three to four others, though that impact varies over time and across states.

Energy industry wages are considerably higher than in other industries. Average nominal earnings for oil and gas employees nationally (extraction and support activities for oil and gas operations) were $1,915 per week in 2025, 53 percent higher than the private sector average of $1,247. When oil prices are high and work is plentiful, overtime pay and bonuses can be substantial. Additionally, for energy sector employees who own company stock, higher dividend payments further boost income. As a result, these higher-earning workers increase consumption, benefiting local communities.

In the U.S., land ownership rights are separable into surface rights and mineral rights. The owner of the mineral rights beneath the surface can lease those rights to an oil producer. Under these arrangements, the lessor receives a portion of production revenue as royalties, commonly referred to as mailbox money. Even Texas farmers without mineral rights often receive compensation for surface access and allowing operations on their land.

Texas has a disproportionately high share of both private mineral rights owners and industry employees. Rising incomes for these groups flow to local communities through various spending and investment channels. Charitable institutions experience revenue fluctuations tied to oil prices, as energy industry giving tends to increase during boom periods.

On the public side, severance taxes and royalties on oil and gas production accounted for more than 9 percent of total state tax revenue in the 2024–25 budget cycle and generated nearly $2 billion of revenue per year for the Permanent University Fund. The endowment funds higher education, largely through the University of Texas and the Texas A&M University systems.

Finally, higher oil prices also increase bank lending. Cash flowing into oil-producing areas boosts bank deposits and supports increased lending. These improvements in bank liquidity support lending to other sectors of the economy.

What is different today?

Production and employment increases this time may be modest, primarily because of uncertainty about how long prices will remain elevated. In addition, limited pipeline capacity for natural gas, equipment shortages and high oilfield efficiency may limit production and employment gains.

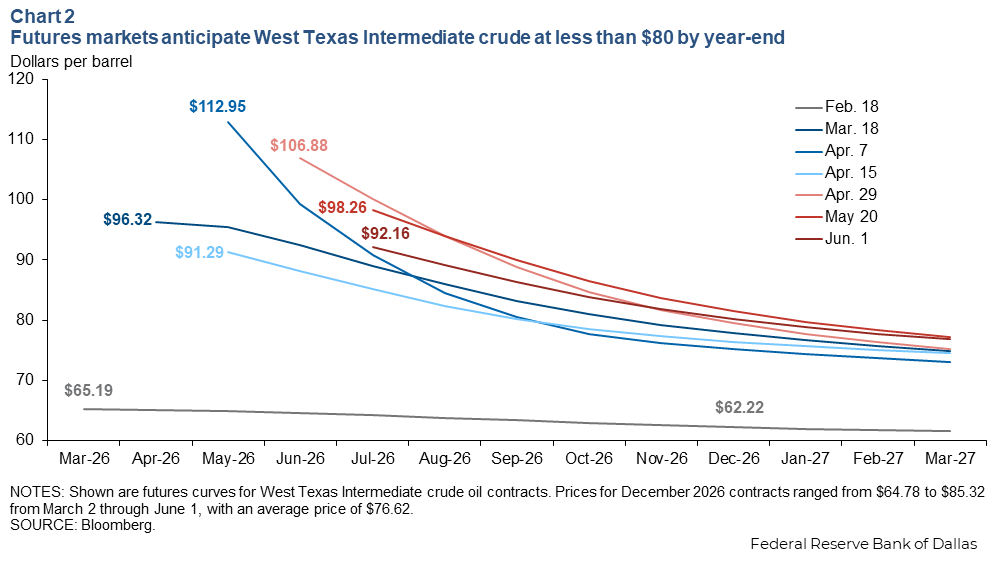

Many exploration and production companies do not expect conflict-driven prices to persist long enough to justify a major production increase. New production requires six to eight months to reach major pipeline networks in response to a price signal. With an average year-end 2026 price expectation of $74 per barrel for WTI, 73 percent of Dallas Fed Energy Survey respondents anticipated no more than 0.25 mb/d of additional production this year.

Producers may choose to hedge the risk of significantly falling prices by buying futures contracts, options, swaps or a combination of instruments to lock in future revenue. However, these market bets can be costly and still carry risk.

Throughout the ongoing Middle East conflict, near-term oil prices have been volatile, though prices for year-end WTI futures contracts have generally converged in a range of $70 to $79 (Chart 2). While futures are not price forecasts, they provide insight into market participants’ expectations. Furthermore, many firms consider futures prices when making investment decisions.

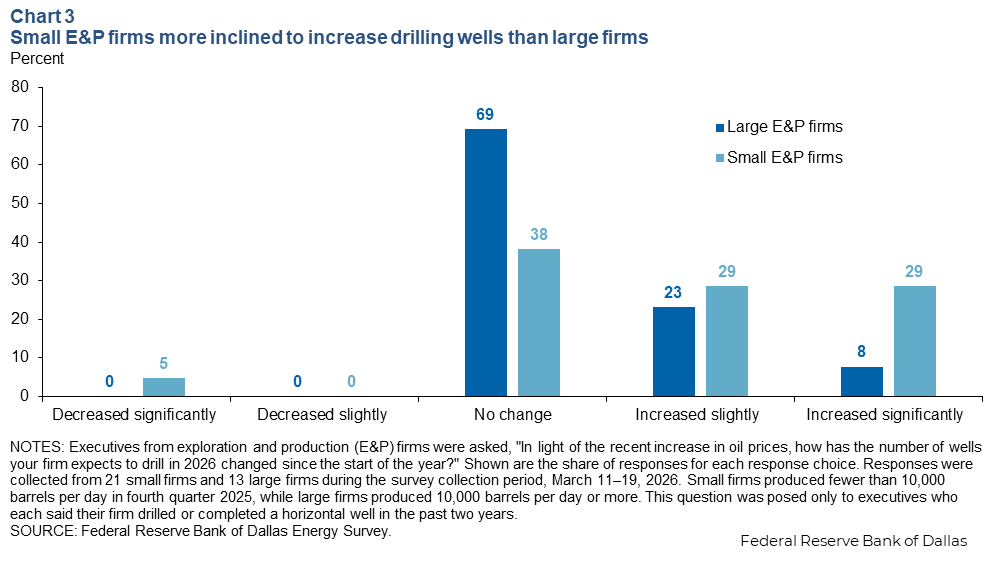

Exploration and production business models have shifted significantly postpandemic. Producers prioritize steady returns for shareholders and are more disciplined with capital management and cost minimization. Large, publicly traded firms appear less willing to risk profitability by chasing higher oil prices with increased debt-financed production. Small exploration and production company respondents to the first-quarter Dallas Fed Energy Survey were more optimistic than their large counterparts about well drilling in 2026 (Chart 3).

Large firms were more likely to report unchanged expectations or not provide an answer to the survey question, suggesting greater uncertainty or risk aversion. Among all survey respondents, 28 percent expected slightly more hiring, while 67 percent anticipated employment to remain either unchanged or to decline from December 2025 to December 2026, according to an update to the first-quarter 2026 Energy Survey.

Until sufficient confidence emerges that producers can deliver new production with adequate profitability, large Texas exploration and production firms will remain focused on maximizing profits and dividends from current operations. In the meantime, firms will likely accelerate drilling completions already underway to add production at the margin and capture higher near-term prices. Thus, the state may still see modest production increases.

Short-run constraints further limit significant production expansion. Every oil well produces natural gas as a byproduct, which can either be captured and sold or released into the atmosphere (venting or flaring). However, the capacity to transport and store natural gas in the Permian Basin is limited. The state’s primary production region has been so constrained that producers have paid customers to take their natural gas—the benchmark Waha natural gas price frequently drops below zero, even during winter.

The weekly price for Waha natural gas averaged –$1.44 per million British thermal units (MMBtu) from the week ended Oct. 3, 2025, through the week ended Feb. 27, 2026. From the first week of March to the last week of May, it averaged –$4.63, and producers at times have paid more than $9 to have gas taken away. Venting and flaring natural gas are regulated by federal and state laws, and many producers have committed to investors and foreign buyers to limit flaring. Without greater capacity to store or transport this natural gas, producers will be limited in their ability to increase oil production.

Oilfield equipment availability is another constraint. Oilfield services firms have operated with compressed margins since the pandemic, and demand has been insufficient to justify excess equipment capacity. Additionally, supply constraints for critical machinery, such as generators to power oilfield operations, limit potential activity. Data centers and commercial developers are major competitors for generators.

Production efficiencies limit workforce demands

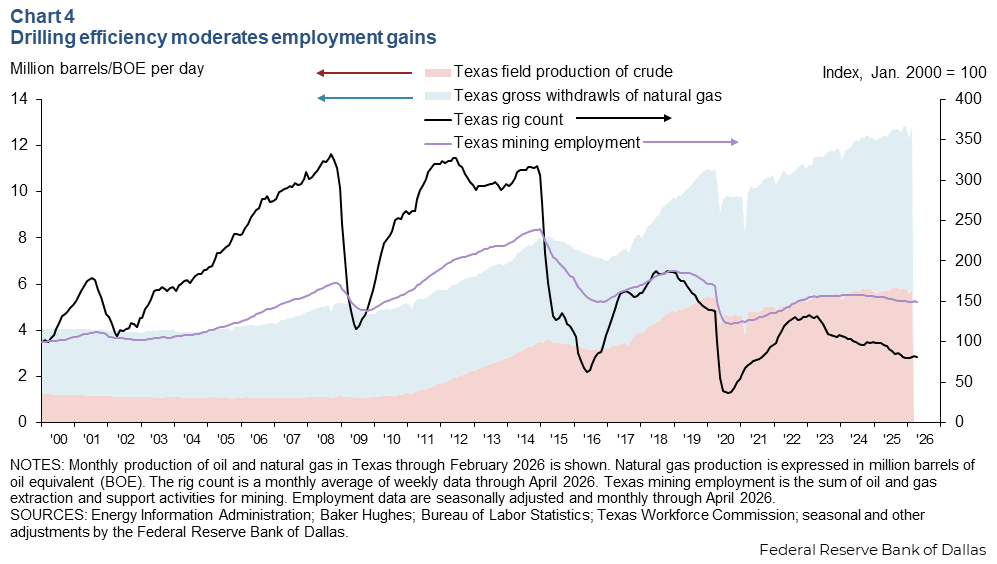

Recent productivity gains limit the employment impact of higher oil prices. Fewer workers are needed to reach increased production targets relative to the 2010s expansion. Continuous innovations in hydraulic fracturing used for shale oil exploration, faster and deeper horizontal drilling, improved well placement and automation have enabled the shrinking energy labor force to expand output dramatically.

From 2006, before the shale boom, to 2025, when the shale drilling industry had matured, state oil production expanded by 435 percent and gas production rose 115 percent. Meanwhile, the number of direct oil and gas mining sector employees grew just 14 percent (Chart 4).

Higher prices likely for a while

Oil is a globally traded commodity. U.S. refineries rely on both domestic and imported inputs to produce refined products for domestic consumption and export. Local markets for oil and refined products are not isolated from the effects of global supply and demand.

Average retail prices for regular gasoline in Texas surged from $2.46 per gallon the week of Feb. 16, 2026, before the Iran conflict, to $3.96 per gallon the week of May 25. For many low- and moderate-income Texans, this 61 percent increase represents a significant burden on household budgets and may force cutbacks in driving or spending, or increased borrowing.

Recent Dallas Fed research finds that a one-quarter closure of the Strait of Hormuz that reduces global oil supply by 15 percent would result in a 0.6 percentage-point boost to year-over-year headline inflation in fourth quarter 2026 and a 0.2 percentage-point drag on GDP. Prolonged closure of the strait pushes oil and fuel prices higher, extends the duration of elevated prices and amplifies the negative macroeconomic effects on the U.S. and global economy.

For now, a lengthy closure is not the base case, or benchmark future scenario, for oil markets or U.S. producers. The boost to domestic capital expenditures and regional hiring by the oil and gas sector will likely be modest. As a result, windfall income from higher profits on existing production will be the primary channel for offsetting the negative effects of higher fuel prices on Texas households and the broader economy.

About the authors

Robert Leigh is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.

Jesse Thompson is a senior business economist at the Houston Branch of the Federal Reserve Bank of Dallas.

Luis Torres is a senior business economist in the San Antonio Branch of the Federal Reserve Bank of Dallas.