Ciudad Juarez retools amid job losses

Ciudad Juarez, Mexico's sixth-largest city and a critical manufacturing hub directly across the border from El Paso, shed approximately 57,500 maquiladora jobs from mid-2023 to mid-2025.

This contraction represents an 18 percent loss of manufacturing workers. It is a byproduct of Juarez’s evolution toward higher value-added manufacturing activity. This development also reflects weakening U.S. demand for products from the area’s longstanding automotive sector, along with increasing labor costs, peso appreciation and higher tariffs.

These pressures have accelerated a structural shift toward automation and away from low-margin, labor-intensive production.

Maquiladoras a key economic driver in northern Mexico

The manufacturing sector plays a vital role in Mexico’s economy, particularly in northern Mexico’s border cities, where the majority of the nation’s manufacturing activity is concentrated in part due to its proximity to the U.S.

Manufacturing facilities that are a part of the IMMEX (Manufacturing, Maquila and Export Services Industry) program, also known as “maquiladoras,” are mostly foreign-owned. They engage in the relatively labor-intensive assembly of intermediate and final goods for export.

Under the program, maquiladoras can import raw materials, components and equipment duty free. These goods are used to produce finished products for export to the U.S., and duties typically are only applied to the value added on products sent back to the U.S. Under terms of the United States–Mexico–Canada Agreement (USMCA) governing most trade between the three signatory countries, additional tariffs may apply if manufacturing components do not meet rules of origin.

Juarez, boasting a population of roughly 1.5 million, has long been a major manufacturing center. The sector accounted for roughly 326,000 jobs, or 65.3 percent of total formal employment in the city, at its recent peak in mid-2023.

This intricate web of manufacturing activity in Juarez is not only vital for Mexico's economic health but also has profound implications for the U.S., especially El Paso. Thriving Juarez manufacturing plants create a ripple effect, generating service-sector jobs across the border in transportation, real estate and professional services.

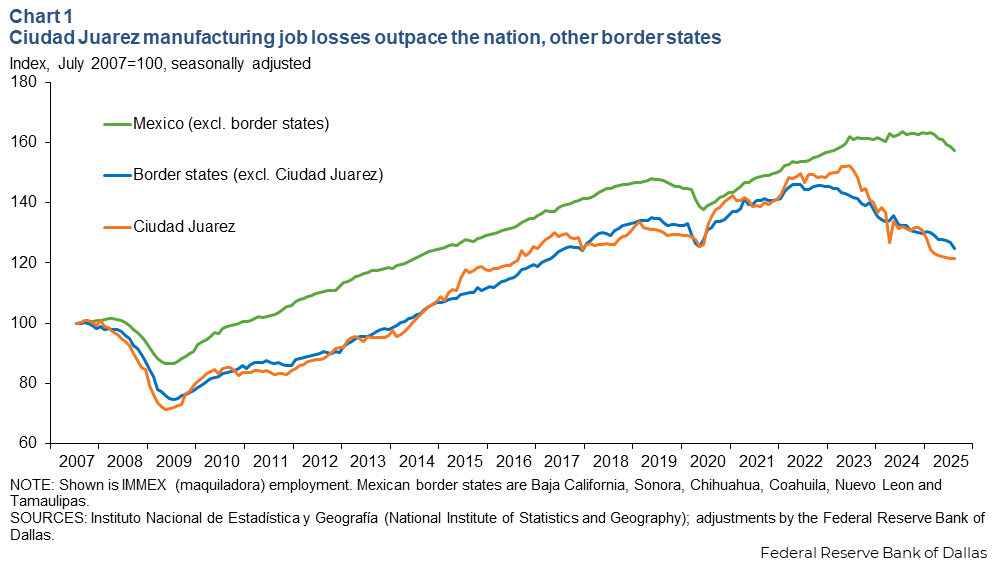

Juarez loses automotive-related manufacturing jobs

The recent maquiladora employment decline, while most pronounced in Juarez, has rippled across major manufacturing hubs throughout northern Mexico (Chart 1).

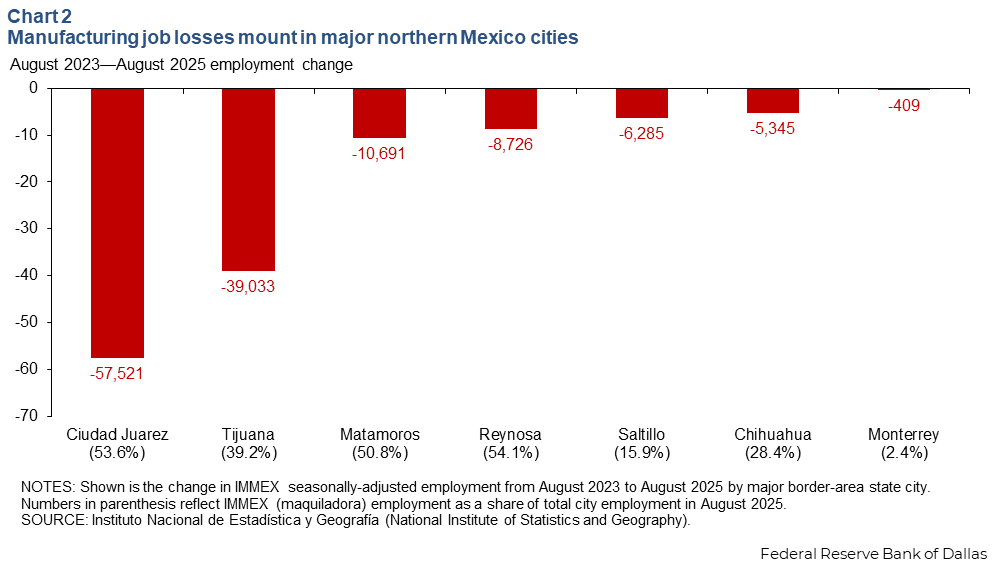

Juarez registered the largest number of job losses from mid-2023 through August 2025 among northern border cities. It was followed by Tijuana, Matamoros and Reynosa (Chart 2). Employment losses have also spread deeper into the northern region, with interior cities such as Chihuahua and Saltillo also recording declines.

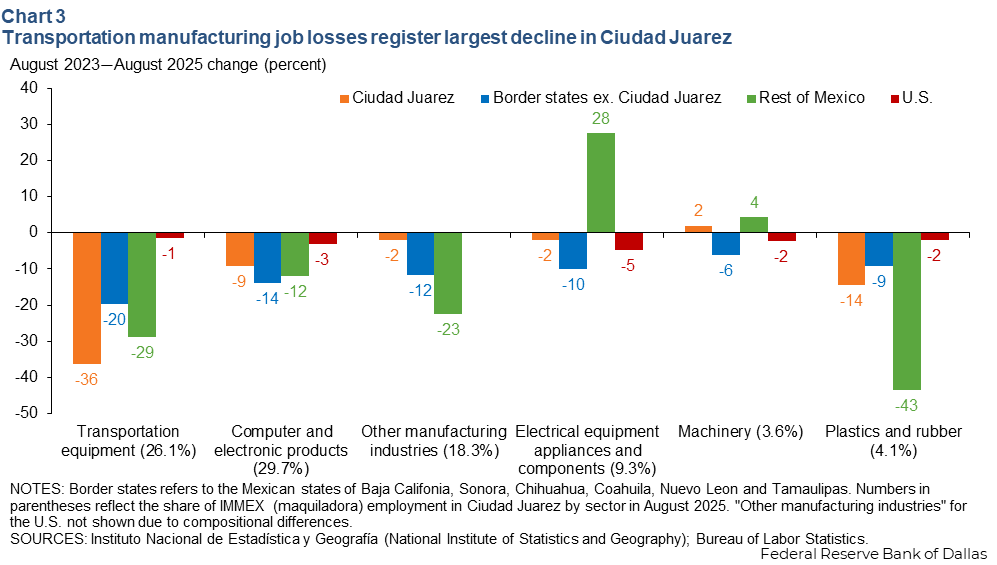

Juarez maquiladora employment fell from 317,000 workers in August 2023 to 259,500 by August 2025. The decline reflects the city’s historical dependence on transportation manufacturing, a sector that employed nearly one-third of the city’s maquiladora workforce in mid-2023 (Chart 3). As the industry contracts, Juarez has been disproportionally affected relative to cities with lesser automotive-related manufacturing, such as Monterrey.

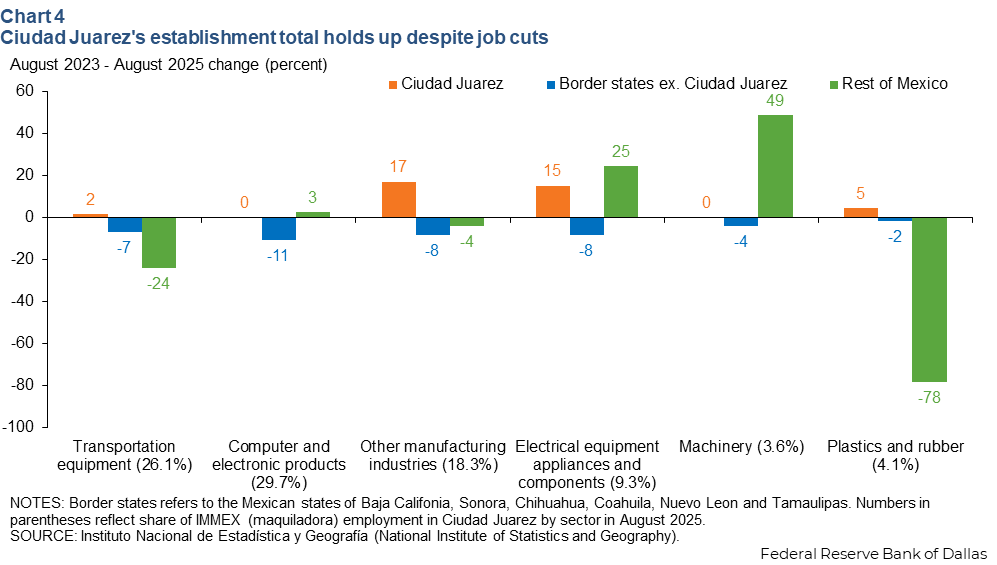

Number of maquiladora plants stable despite employment declines

While Juarez has experienced substantial declines in maquiladora employment, the number of maquiladoras has remained steady or even increased in some sectors (Chart 4).

This is a likely result of ongoing shifts toward automation, as companies look to maintain or expand their physical footprints while reducing headcounts. Many firms in Juarez are pivoting towards increasingly leaner operations, investing in advanced manufacturing technologies, robotics and automated production lines requiring significantly fewer employees.

In other regions of Mexico, employment declines generally correspond with establishment closures, suggesting that despite workforce contractions, Juarez remains a key manufacturing hub. Juarez is experiencing particularly strong growth in electrical equipment, driven by expanding medical device and electronics operations.

Slowing business cycle, rising costs and industrial transition

Mexican manufacturers depend on U.S. demand, resulting in synchronized business cycles in the two countries' manufacturing sectors.

U.S. industrial production slipped 0.2 percent and manufacturing 1.0 percent from June 2023 to January 2025. Mexican industrial production dipped 0.8 percent and manufacturing fell 0.7 percent during the period, and maquiladora employment contracted after initially growing.

Automotive manufacturing in particular has experienced a notable slowdown, with production declines affecting several automakers despite overall industry sales growth. The auto industry has suffered from excessive inventory levels, shifting electric vehicle demand patterns, intensifying competition from Chinese manufacturers and, more recently, rising tariff-related costs.

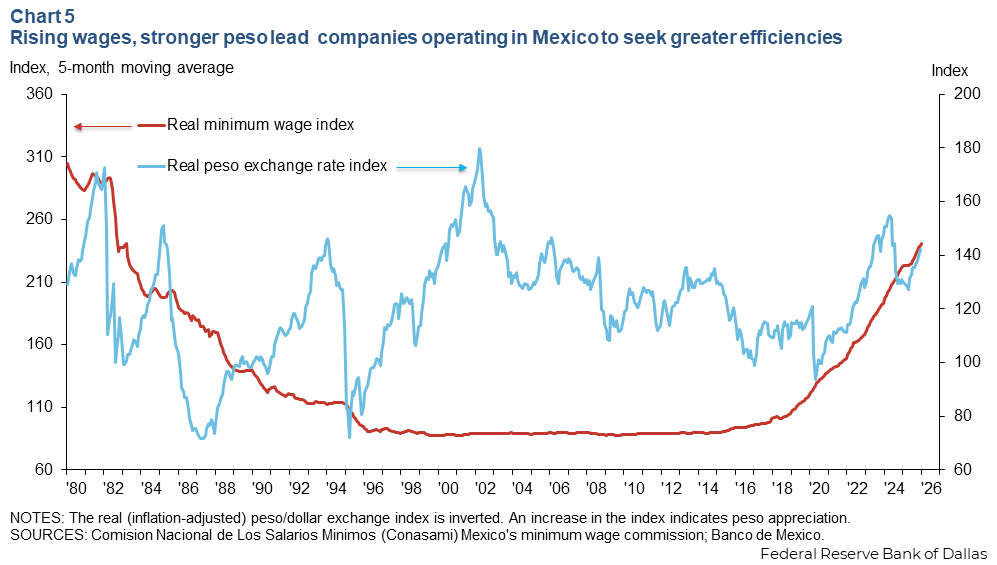

Additionally, Mexican labor costs have increased as part of annual adjustments to the nation’s minimum wage since 2019. The minimum wage serves as a reference point that drives other labor costs, including in the maquiladoras and elsewhere in the formal sector.

The minimum wage increases were codified under former President Andres Manuel Lopez Obrador. Before 2019, Mexico’s real (inflation-adjusted) minimum wage was near 1994 levels (Chart 5).

A virtually stagnant real minimum wage beginning in 2001 coincided with exchange rate volatility, including periods of significant peso depreciation. The real minimum wage grew at an average annual rate of just 0.7 percent from 2001 through 2018, while the peso depreciated about 1.4 percent annually during the period.

Companies operating maquiladoras largely earn revenue in dollars while paying local operating costs (labor, rent, utilities) in pesos. The firms obtained additional benefit from the weak peso and stagnant wages in the 2001–18 period.

Beginning with the Lopez Obrador administration, average yearly growth in the real minimum wage has been 12 percent, while the peso appreciated 4.1 percent a year from 2019 to 2025. The moves eroded some of the maquiladoras’ competitive cost advantage, notably in 2023 when wages increased 14.8 percent and the peso appreciated 15.5 percent.

Wages in Juarez maquiladoras increased 87 percent from August 2018 to August 2025, sending some low-margin, labor-intensive operations—particularly vehicle wire harness manufacturing—to southern Mexico or Central America locations, such as Honduras, with lower labor costs.

U.S. tariffs on some non-USMCA-compliant inputs have added to rising maquiladora costs. The Mexican government took its own actions that further increased costs and disrupted operations. Officials significantly intensified audits of companies operating under the IMMEX program to curb tax evasion and ensure regulatory compliance.

Amid this backdrop, Juarez has experienced a structural shift toward more high-skill, capital-intensive industries, partially driven by rising wages and robust demand attributable to the artificial intelligence-related U.S. data center build-out. Electronics firms, in particular, have also moved to reshore or nearshore production to Mexico as part of broader strategies to diversify supply chains away from Asia.

Transitioning toward a new manufacturing base

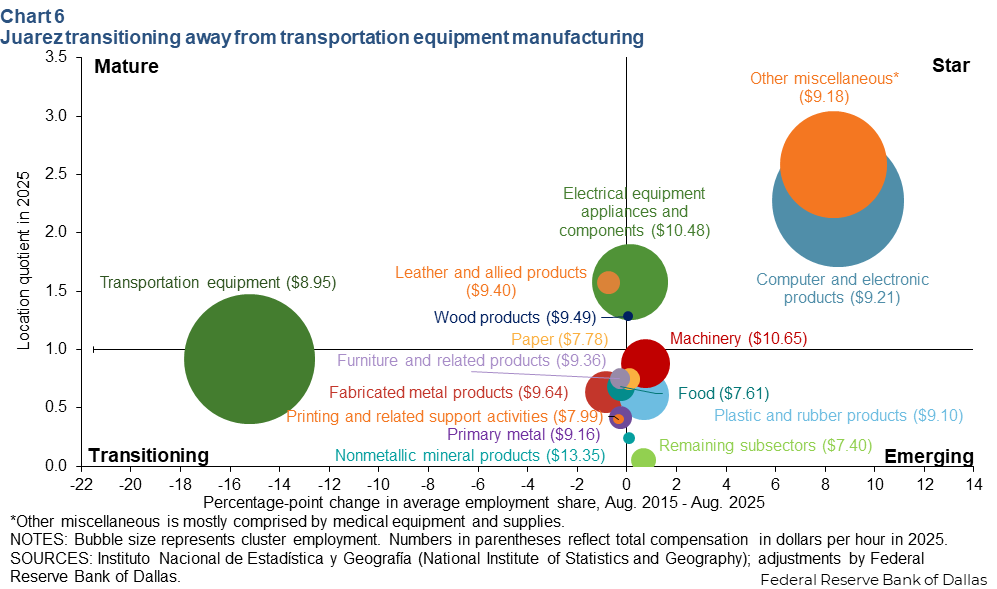

Cluster analysis helps depict Juarez’s evolving manufacturing landscape. An area typically has an economic base that consists of several dominant industry clusters. These clusters typically exceed the national average in their share of employment, output or earnings.

Location quotients (LQs), which compare the relative concentration of industry clusters locally and nationally, are one way of assessing these key drivers in an area’s economy. An LQ exceeding 1 indicates that a specific industry cluster is more dominant locally than nationally. LQs are calculated using maquiladora industry cluster employment. Industry cluster growth is measured by the percentage-point change in its share of local employment between 2015 and 2025.

Chart 6 plots industry cluster LQs and growth for maquiladora employment in Juarez.

Clusters in the top half of the chart, such as computer and electronic products, other miscellaneous and transportation equipment are referred to as base clusters. They have a larger share of local employment relative to the nation and, thus, an LQ exceeding 1. A base cluster is usually vital to an area’s economy and can be expanding relatively rapidly (star) or growing slowly or declining (mature). Those in the bottom half are less dominant locally than nationally; hence, they have an LQ below 1. “Emerging” clusters, such as machinery, are relatively fast-growing, while those growing slowly or declining are termed “transitioning.”

Juarez is transitioning from low value-added transportation equipment manufacturing and assembly. These products are often highly sensitive to price competition and tariffs, and their manufacture is frequently considered for relocation.

While the city has continued to grow its medical device manufacturing base, which makes up the majority of the other miscellaneous cluster, the local economy is also evolving towards higher value-added electronics manufacturing, including servers, integrated circuits, central processing units and networking equipment, to support U.S. data center construction.

In 2024, the Mexican state of Chihuahua and its principal city of Juarez accounted for almost two-thirds of Mexico's rapidly growing exports of automatic data processing machines used in data centers.

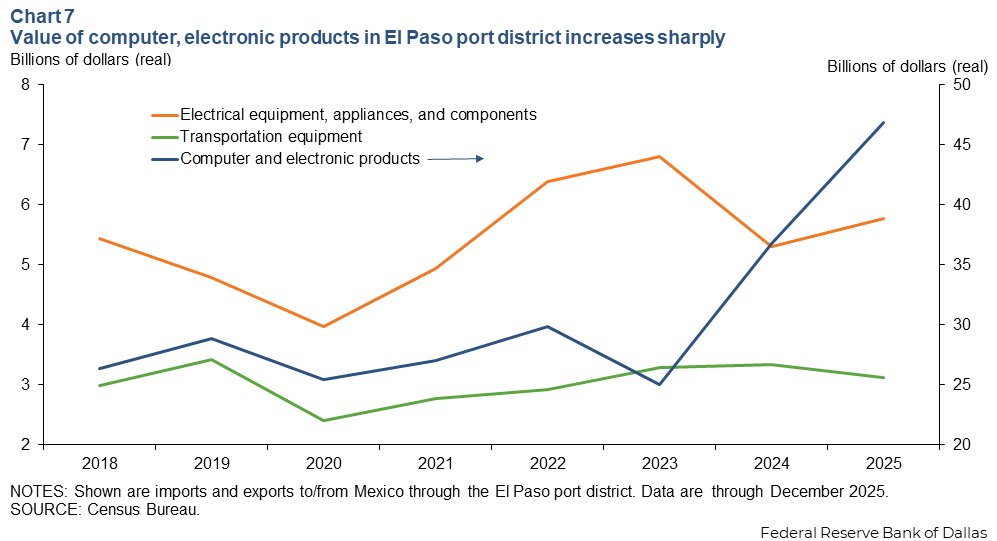

Data from the El Paso trade district, which largely covers ports of entry from El Paso through Santa Teresa, N.M., provide further evidence of Juarez’s transitioning manufacturing landscape. Of the top three commodities flowing through the trade district, computer and electronic products have grown impressively in recent years. Trade volumes surged 87 percent from 2023 to 2025 (Chart 7). In contrast, transportation equipment, historically the cornerstone of Juarez's industrial economy, declined by 5 percent over the period.

Juarez experienced a earlier maquiladora transition in 2002 after China joined the World Trade Organization. China took over low value-added, labor-intensive manufacturing such as apparel, textiles and furniture. Commoditized and highly price-sensitive electronics such as printed circuit boards, mobile phones and disk drives also migrated to lower-wage countries.

Rather than collapsing, Juarez's manufacturing sector evolved. Higher value-added manufacturing that leveraged Mexico's proximity to the U.S. market not only remained but expanded. The city retained and grew production of items where frequent design changes, quality requirements, just-in-time delivery or high weight-to-value ratios mattered more than labor costs, including high-end flat screen TVs and medical instruments and supplies.

El Paso-Juarez faces future challenges

While the loss of employment in Juarez is significant, the city is evolving toward higher value-added manufacturing positions, largely providing equipment for the data center build-out in the U.S.

Texas has emerged as a national leader in data center construction, second only to Virginia, with $10 billion in such construction in 2025. El Paso is part of this expansion, with Meta building a $1.5 billion, 1-gigawatt AI-focused data center in the city, and the Project Jupiter data center taking shape just across the state line in Las Cruces, N.M. More recently, the Army announced plans for a self-contained data center on the grounds of Fort Bliss to be completed by 2027. Taken together, these facilities require massive amounts of sophisticated hardware that create sustained demand for the types of electronics Juarez increasingly produces.

As Juarez ramps up, El Paso stands to benefit through both higher-value trade flows and the potential revival of the twin-plant model originally envisioned under the North American Free Trade Agreement of 1994 (the predecessor to the USMCA).

Taiwan manufacturers are leading this trend, with Wiwynn providing a prime example. It expanded Juarez production of data center servers in 2024 and 2025. The company also announced a $150 million investment in a manufacturing and testing facility across the border in El Paso.

Still, challenges remain. Just as Juarez successfully transitioned from apparel and basic electronics to automotive parts and medical devices two decades ago, it now seeks a more sophisticated manufacturing profile. But there is a difference this time. Uncertainty about the much-anticipated renegotiation of USMCA during 2026 could lead to less manufacturing investment along the Mexican border.

Simultaneously, the Mexican government has sought to protect local production, taking aim at Chinese and some other Asia manufacturers seeking to bypass U.S. tariffs. At the start of 2026, Mexico imposed tariffs of 20–35 percent (and up to 50 percent on selected items) on imports from countries without free-trade agreements with Mexico, such as China, India, South Korea, Thailand and Indonesia. These tariffs apply to automobiles, auto parts, textiles, clothing and plastics.

These new tariffs could raise input costs and disrupt supply chains, given that it would take time to develop local suppliers in the U.S. and Mexico.

The long-run transition to higher-skilled jobs means less demand for low-skill workers, which so far has hindered job growth and is behind Juarez’s declining employment numbers. Over time, the El Paso-Juarez region needs to develop a workforce better aligned with its emerging industrial base to remain one of North America's most significant manufacturing and trade corridors.

About the authors

Isabel Brizuela is a business economist in the Research Department of the Federal Reserve Bank of Dallas.

Jesus Cañas is a senior business economist in the Research Department of the Federal Reserve Bank of Dallas.

Luis Torres is a senior business economist in the San Antonio Branch of the Federal Reserve Bank of Dallas.

Diego Morales-Burnett is a research analyst in the Research Department at the Federal Reserve Bank of Dallas.